I. Introduction

When asked about raising taxes on the wealthy to fund New York State’s response to the coronavirus pandemic, Governor Andrew Cuomo has said “I don’t know how you raise taxes on people who are out of work and their businesses are closed because government needs more funding.”[1] It is not the only time that Cuomo has implied that the ultra-rich have been as ravaged by the pandemic as working class New Yorkers. Cuomo has called coronavirus “the great equalizer”[2] and has said that “everyone is suffering on a lot of levels.”[3]

However, Cuomo’s assertions about everyone suffering are not borne out by data.

While pre-existing structural inequities have caused the disease and its side-effects to devastate New York’s working class communities and communities of color, the state’s billionaires have increased their wealth substantially over the course of the pandemic.

PAI’s analysis of Forbes wealth data has found that:

- New York State’s 118 billionaires increased their net worth by an estimated $44.9 billion, or 8.6%, from March 18th to May 15th. Even amidst the wreckage of the pandemic, the billionaires’ collective net worth has rebounded and surged to $566 billion.

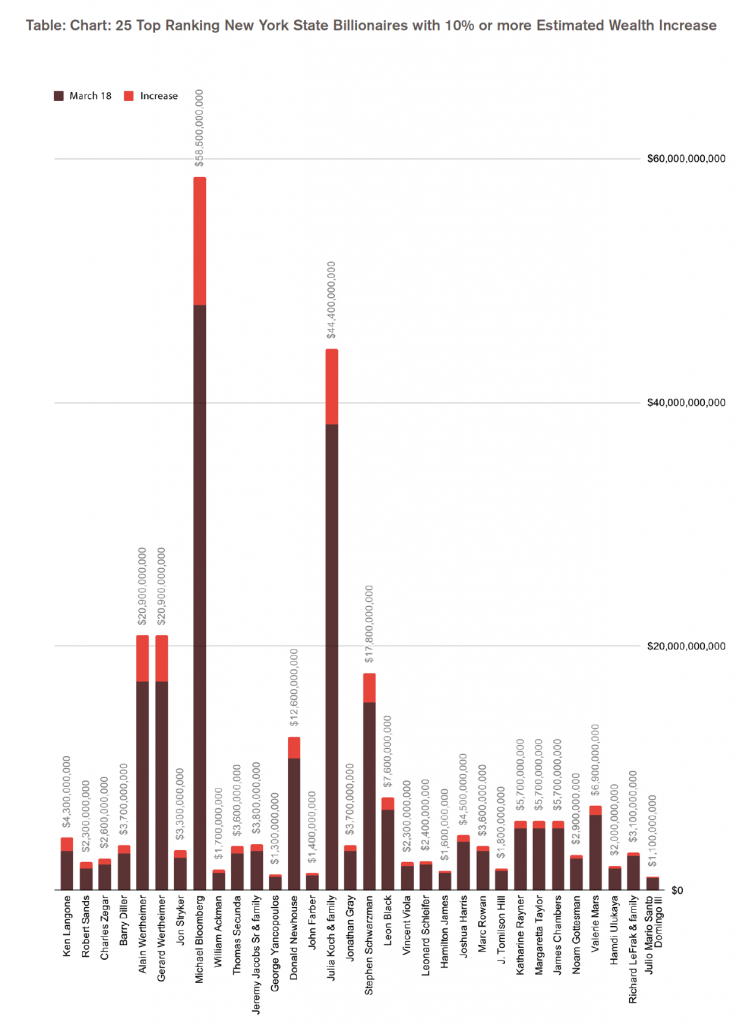

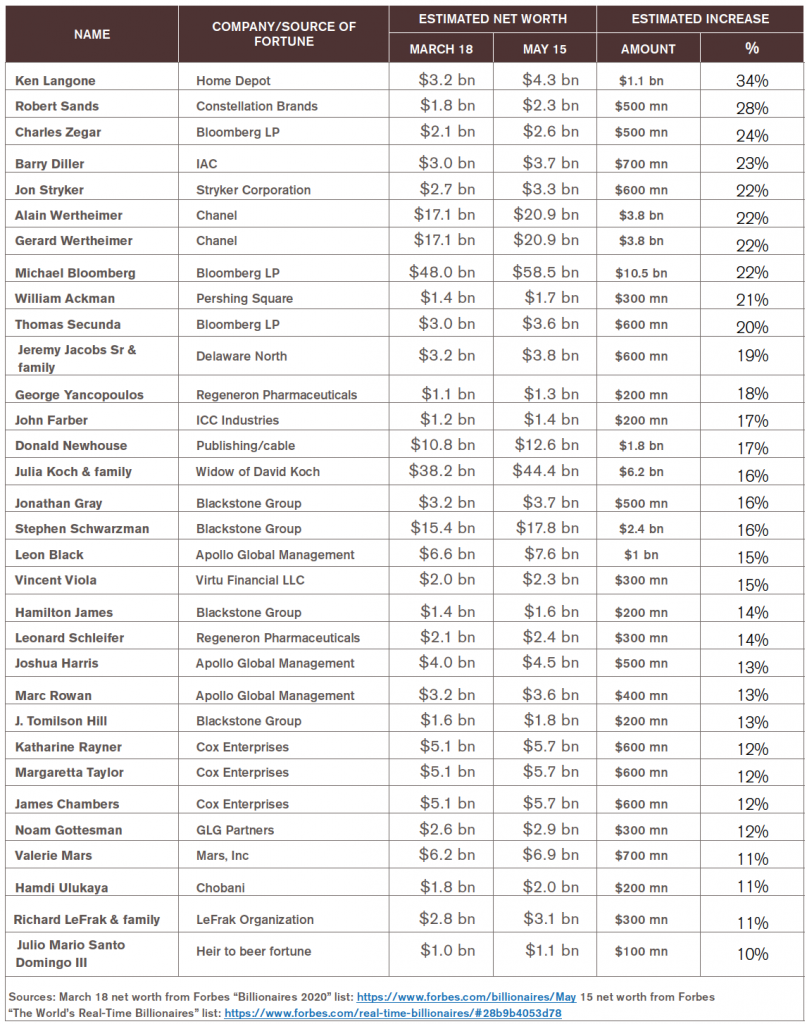

- Thirty-two of the state’s billionaires have increased their wealth by 10% or more. The estimated net worth of the wealthiest New Yorker, Michael Bloomberg, now stands at $58.5 billion, a $10.5 billion or 22% increase since March 18th.

- Since 2019, the number of billionaires in New York State has increased from 112 to 118. New York State billionaires added to Forbes’ billionaires list in 2020 include Wall Street money managers David Golub, Lawrence Golub, and Wesley Edens.

Over the same period, as billionaires have added nearly $45 billion to their wealth, people of color and working class people in New York have faced a very different picture:

- More than 2 million New Yorkers have lost their jobs. According to the NYS Department of Labor, from the week that ended March 21 through the week that ended May 9, people filed 2,026,869 initial unemployment claims in New York.[4]

- Working class people and people of color are far more likely to contract the coronavirus, be hospitalized, and die. An analysis by The City found that neighborhoods in New York City with public housing developments had a 30% higher rate of COVID-19 hospitalization than surrounding neighborhoods.[5] In Buffalo, the region’s five majority-Black zip codes have infection rates 88% higher than in the rest of Erie County according to the Buffalo News.[6] The American Public Media Research Lab found that Latino Americans are 1.2 times more likely and Black Americans are 2.6 times more likely to die from COVID-19 than White Americans.[7]

In this context, Governor Cuomo’s policy orientation amounts to a pandemic wealthcare plan. Cuomo has prioritized the wealth and influence of billionaires – many of whom are his donors[8] – over the physical well-being of the most vulnerable communities that he represents:

- Cuomo has refused to enact measures that would address the crisis for working class people. Cuomo has rejected raising taxes on billionaires to pay for vital social infrastructure and canceling rent and mortgage payments while rolling back bail reform and proposing cuts to public services.

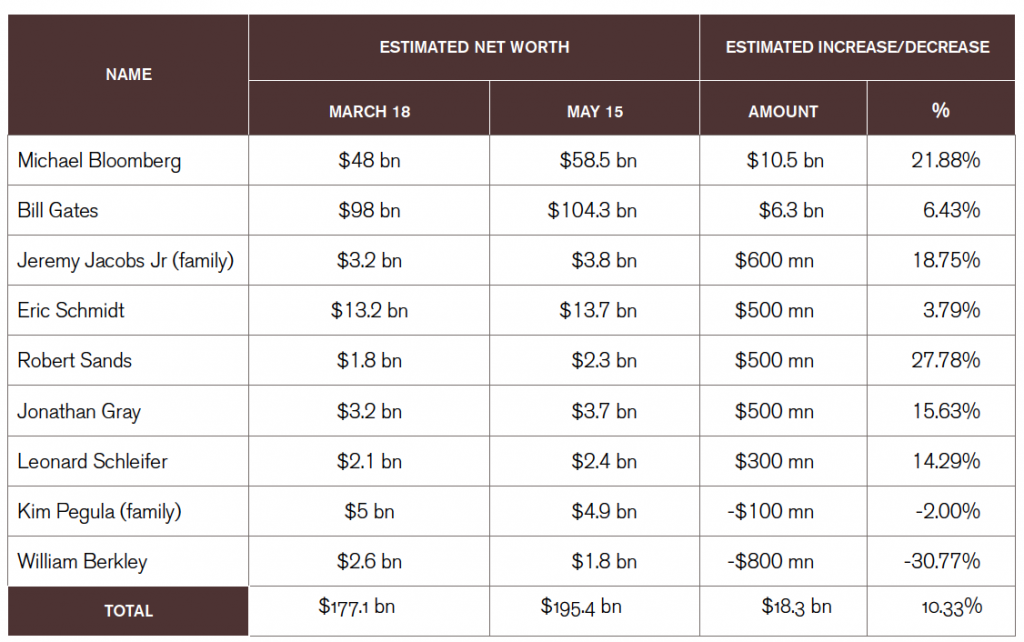

- Cuomo has put billionaires in charge of shaping New York’s response to the pandemic and economic recovery. Cuomo has tapped Michael Bloomberg to create a contact tracing program for the state, Bill Gates to “reimagine” New York’s public education system, and Eric Schmidt to “reimagine” telehealth and internet access. Cuomo has also appointed six billionaires – Kim Pegula, Jeremy Jacobs Jr, Jonathan Gray, Leonard Schleifer, Robert Sands, and William Berkley – to his re-opening advisory board.[9] The aggregate net worth of the nine billionaires has increased over 10%, by $18.3 billion, from March 18th to May 15th according to our analysis of Forbes billionaire data.

The following report shows how New York State billionaires’ wealth has surged, identifies features of Cuomo’s pandemic wealthcare plan, and profiles key billionaires that have expanded their fortunes, mistreated workers, and landed influential policy planning roles during the pandemic.

II. New York State Billionaire Wealth Has Surged During the Pandemic

New York State’s billionaires have gotten much wealthier over the course of the COVID-19 pandemic, even as the health and economic crisis caused by the pandemic has devastated much of the state.

PAI analyzed Forbes billionaire data and found that the estimated net worth of the New York State billionaires identified by Forbes in its 2020 billionaire list increased substantially between March 18th and May 15th.[10]

During that period – as hundreds of thousands of New Yorkers got sick and over 20,000 died from COVID-19, over 2 million people lost their jobs, and the state’s schools and many of its small businesses shut down their operations – New York State billionaires’ aggregate net worth increased by an estimated $44.9 billion, or 8.6%.

Furthermore, Forbes’ 2020 billionaire list identifies 118 New York State billionaires, up from the 112 New York State billionaires it identified in 2019. Combined, the 118 billionaires had a net worth of $566.4 billion as of May 15, 2020.

The estimated net worth of the wealthiest New Yorker, Michael Bloomberg, now stands at $58.5 billion, a $10.5 billion or 22% increase since March 18th. Additionally, 32 of the state’s billionaires have increased their wealth by 10% or more (a table is included below). Several of these billionaires are profiled in the sections that follow.

To conduct the analysis, we followed a methodology first developed by the Institute for Policy Studies (IPS) to track overall increases in US billionaire wealth during the pandemic, applying it to the billionaires Forbes identifies as New York State residents. IPS’s “Billionaire Bonanza 2020” report has received extensive media coverage.[11] IPS continues to provide updates on billionaire wealth increases nationally.[12]

III. Cuomo’s COVID-19 Wealthcare Plan

Though Andrew Cuomo has stressed in his public statements the need for all New Yorkers to do their part to save lives during the outbreak and to recover afterwards, in deed he has worked to protect the wealth and status of New York’s richest residents and business owners.

Below are some of the key ways that Governor Cuomo has protected billionaire wealth at public expense.

Refusing to tax the rich

Even before the coronavirus pandemic reached the United States, Cuomo has faced calls to tax the ultra-rich in order to provide adequate housing, public education, and other essential services to all New Yorkers.

Community and labor groups as well as progressive legislators have proposed more than a dozen bills to raise revenues for vital public services.[13] Proposals range from repealing tax breaks that primarily benefit the wealthy – like the stock transfer tax refund and Cuomo’s yachts and jets sales tax break – to taxing mostly-vacant homes owned by the ultra-wealthy to taxing billionaire wealth outright. Advocates estimate that 14 “tax-the-rich” bills would generate an additional $35 billion per year in state revenue that could be spent on social and supportive housing, public education, public transit and other essential social infrastructure.

Cuomo has dismissed these proposals out of hand, insisting instead on more budget cuts for state programs upon which the people most severely impacted by the coronavirus pandemic depend.[14]

Cuts to public services

New York began 2020 facing a $6 billion budget deficit driven in large part by Cuomo’s austerity budgets and tax breaks for the ultra-wealthy. Rather than raising revenues by taxing the wealthiest New York residents and businesses to cover this gap, Cuomo convened a Medicaid Redesign Team which recommended hundreds of millions of dollars in cuts to the state-administered program that insures people who cannot afford to buy health insurance on the private market.[15]

Cuomo was so adamant about his Medicaid cuts that he threatened to turn down $6.7 billion in federal coronavirus aid because it would have prevented him from implementing the cuts.[16]

As the crisis has drawn on and worsened over the past two months, Cuomo has threatened to cut more.

In his state budget proposal, Cuomo demanded the ability to implement rolling budget cuts throughout the year due to the coronavirus pandemic.[17] The legislature granted Cuomo this authority as it rushed to enact a budget without the usual negotiation and debate to ensure that money was appropriated to fund governmental agencies. The budget also included the Medicaid cuts planned by the Medicaid Redesign Team, though it delayed those cuts in order to take advantage of the federal aid Cuomo had threatened to turn down.[18]

In his financial plan released April 26, Cuomo announced his first round of $10.1 billion in cuts, including an $8.2 billion reduction in aid to localities.[19] Cuomo has not released details of these planned cuts yet, but warned that he intended to cut “funding for health care, K-12 schools, and higher education as well as support for local governments, public transit systems, and the State’s not-for-profit partners who deliver critical services to the most vulnerable New Yorkers.”[20]

Refusing to cancel rent

From the early days of the pandemic’s spread in New York, housing justice and tenant advocates have prevailed upon Cuomo to use his extraordinary emergency powers to cancel rent and mortgage collections in New York. Rather than granting relief to tenants – who make up 67.3% of New York City residents and 46.1% of all New Yorkers[21] – Cuomo enacted a temporary eviction moratorium, which he later scaled back.

On March 20, Cuomo issued an executive order that put a 90-day moratorium on evictions and foreclosures in the state, a half-measure that provided little relief to tenants who cannot make rent during the crisis.[22] While Cuomo’s moratorium means that landlords cannot force renters from their homes while it is in effect, tenants still owe that rent and can be evicted as soon as the moratorium is lifted.

After issuing the eviction moratorium with no rent relief, Cuomo ducked questions about the incomplete relief provided by his order and cracked jokes about tenants’ hardships.

At a March 22 press conference, Cuomo proclaimed “we took care of the rent issue in New York,” but when asked about rent relief, reiterated that tenants cannot be evicted for not paying rent without addressing the issue of rent after the end of the moratorium.[23] Later in the month, when asked about the extent of rent relief he planned to offer, Cuomo joked that his daughters had stopped paying him rent.[24]

On May 7, Cuomo issued an order that extended the eviction moratorium until August for some, but critically scaled back protection to only those “eligible for unemployment insurance or benefits under state or federal law or otherwise facing financial hardship” due to the pandemic.[25]

Cuomo’s new order has the effect of allowing landlords to attempt to evict tenants and putting the onus on renters – who have fewer legal resources than landlords – to prove their hardship.

Rolling back bail reform

Jails and prisons in New York have become hot-spots of contagion as incarcerated people are tightly packed into small spaces and denied access to personal protective equipment. Rather than releasing as many incarcerated people as possible to mitigate the spread of the disease, Cuomo has turned to prison labor to produce hand sanitizer and face masks for use during the pandemic and has used coronavirus as a pretext for rolling back bail reforms passed in 2019.

As of May 14, 445 incarcerated people and 1,194 staff in New York’s prisons have tested positive for the coronavirus, with 16 incarcerated people and four prison staff dying from COVID-19.[26]

According to the group Release Aging People in Prison, the Department of Corrections and Community Supervision has tested less than 2% of the prison population and released less than one half of one percent of incarcerated people.[27] The New York Daily News reported that 80% of the people who died in New York’s jails and prisons since the outbreak of the coronavirus have been people of color.[28]

While other countries and states have released people from prisons at much higher rates, Cuomo has taken action during the pandemic to put more poor people in jail. In the state budget, which was passed in a rush in early April due to the pandemic, Cuomo and the state legislature rolled back bail reforms passed in 2019 which had just taken effect in January 2020.[29]

The 2019 reforms eliminated bail for a swath of criminal offenses, allowing people charged but not yet convicted of crimes, to await trial outside jail regardless of their financial circumstances. The reform faced intense opposition from police, district attorneys, and the right-wing, and even after it passed, there was a coordinated effort to kill the reforms.[30]

Cuomo’s 2020 budget, which was passed in haste without the usual input from the legislature, added a number of criminal offenses back to the list of those where bail could be set, effectively conditioning freedom before trial for people charged with those offenses on their ability to pay.

Putting billionaires in charge of recovery

Beyond just protecting their wealth during the coronavirus pandemic, Governor Cuomo has put billionaires in charge of setting state policy.

On March 23, Cuomo announced that he was putting two executives at billionaire-owned investment firms – William Mulrow of Blackstone and Steven M Cohen of McAndrews & Forbes – in charge of New York’s economic recovery.[31]

The full list of members of Cuomo’s “New York Forward Re-Opening Advisory Board,” released April 28, included an additional six billionaires: Kim Pegula, Jeremy Jacobs Jr, Jonathan Gray, Robert Sands, William Berkley and Leonard Schleifer.[32]

On April 22, Cuomo announced that he was tapping media billionaire and former presidential candidate Michael Bloomberg to create a contact tracing program for the state.[33]

Then on May 5, Cuomo declared that he was engaging the Bill and Melinda Gates Foundation to “reimagine” New York’s public education system.[34] The next day, Cuomo announced that former Google CEO Eric Schmidt would lead a new commission to “reimagine” telehealth and internet access.[35]

Forbes’ estimated net worth of the nine billionaires tasked with recovery tasks has increased by 10.3%, or $18.3 billion, from March 18 to May 15.

IV. Protecting Pandemic Profiteers

As the COVID-19 pandemic rages on, the seven New York billionaires profiled in this section have fired tens of thousands of workers without pay, scolded people struggling to pay rent, and found ways to scoop up even more assets and profit from the crisis. Several of them now sit on his powerful re-opening advisory board.

Bill Ackman

Net worth: $1.7 billion

Wealth increase during pandemic: $300 million

Hedge funder Bill Ackman, the founder and CEO of Pershing Square Capital Management made $2.6 billion from the coronavirus outbreak by investing in credit default swaps – financial instruments that work like insurance contracts for corporate debt – just before the shutdown.[36] Ackman’s investments were bets that the pandemic would cause a general economic downtown.

On March 18th Ackman went to Twitter to urge Trump to close the borders and put Americans on an “extended spring break.”[37] He then called in to CNBC to continue to implore for a shutdown, saying that he’d had a nightmare about the infectious spread of the virus.[38] He claimed to be “bullish” on stocks, detailing what he was buying, but he did not disclose that he was also betting that the markets would tank.

As of May 15, Ackman’s personal net worth had increased by $300 million – 21.1% – according to Forbes data.

Ackman, who has praised Governor Cuomo’s handling of the shutdown, is also a major donor to Cuomo, contributing $96,000 to his campaigns from 2008 to 2013.

Carl Icahn

Net worth: $17.6 billion

Wealth increase during pandemic: $700 million

Billionaire investor Carl Icahn is positioned to profit significantly from the coronavirus outbreak thanks to a $5 billion bet against commercial real estate.[39] Icahn’s short bet – a gamble that malls and other commercial real estate businesses will default on their mortgages – jumped from $400 million in November 2019 to $5 billion – 25% of his total assets – in March 2020.[40]

Since March 18, Icahn’s net worth has increased by $700 million.

Together with his wife Gail Golden, Icahn has contributed $125,000 to Governor Cuomo from 2006 to 2013. The couple are also generous donors to Icahn’s longtime friend Donald Trump, giving $250,000 to Trump Victory and $10,800 to Trump’s campaign account.

Nelson Peltz

Net worth: $1.6 billion

Wealth increase during pandemic: $100 million

Nelson Peltz is the co-founder and CEO of Trian Partners, a hedge fund that oversees $11 billion in assets. Trian Partners is reportedly already circling companies that are hurting due to shelter-in-place and other restrictions, looking to “plow large sums of money” into these companies to snap up high dividend stock and “warrants to buy new stock at a cheaper rate.”[41]

Peltz has come under fire for his role as a major investor and board member at Wendy’s, which is refusing to join the Fair Food Program, a program that ensures better wages and safer working conditions for Florida’s tomato pickers.[42]

Peltz has donated $32,000 to Cuomo from 2006 to 2015. He is also a major Trump donor, giving a total of $85,800 across several donations to Trump’s campaign committee and joint fundraising committee

Leonard Schleifer

Net worth: $2.2 billion

Wealth increase during pandemic: $300 million

Leonard Schleifer is the billionaire co-founder of Regeneron Pharmaceuticals, a New York-based biotech firm that is currently testing whether its arthritis drug is effective against COVID-19.[43] If the drug proves effective it would be a boon for the company but Schleifer is already seeing personal gain. His net worth rose from $1.98 billion to $2.2 billion in less than two months during the pandemic.[44]

Schleifer’s son Adam Schleifer, who is currently running for Congress in New York’s 17th Congressional District to replace Rep. Nita Lowey, reported his own net worth at $31 million.[45]

Leonard Schleifer and his wife Harriet Partel Schlefier donated a combined $11,500 to Cuomo from 2013 to 2017. Now Schleifer is sitting on the Governor’s re-opening advisory board.

Stephen Ross

Net worth: $7.6 billion

Wealth increase during pandemic: $0

Related Companies founder and chairman Stephen Ross is worth $7.6 billion, owns the Miami Dolphins NFL franchise, the high-end workout chains Soulcycle and Equinox, and a number of restaurants.[46] Related Companies is a massive real estate developer with a $60 billion real estate portfolio that includes Hudson Yards and the Time Warner Center in New York. The company also holds the largest private portfolio of affordable housing units with more than 60,000 units across the US.[47]

On April 6th Related Companies CEO Jeff Blau took to the airwaves on CNBC to scold tenants for not paying rent, saying that COVID-19 pandemic “is not an excuse for people to not pay rent.”[48] Notably two days later, Equinox notified the landlords who rent to its many locations that it was refusing to pay April rent because the gyms had been shut down due to social distancing guidance.[49]

Ross is a longtime supporter of Governor Cuomo, giving $80,000 throughout his career beginning with a $25,000 donation during Cuomo’s run for Attorney General in 2005.[50] Ross and The Related Companies have donated $28,000 to the Real Estate Board PAC since 2009. The PAC has donated over $147,000 to Cuomo over the years.[51]

Ross is also a longtime friend of fellow New York developer Donald Trump. Last year Ross hosted a swanky fundraiser for Trump at a Hampton’s mansion where guests could pay as much as $250,000 for a photo op with the President.[52] Recently it was reported that Ross was able to convince Trump to include gyms in the list of businesses allowed to operate under the first phase of the plan for re-opening state economies – a move that has baffled public health experts.[53]

Kim & Terry Pegula

Net worth: $5 billion

Wealth increase during pandemic: -$100 million

Kim and Terry Pegula made billions in fracking in Pennsylvania during the shale boom and are now owners of several Western New York sports teams including the Buffalo Bills NFL team and Buffalo Sabres NHL team. The Pegulas are among the ranks of NHL and NFL team owners who are unabashedly hanging their workers out to dry during the pandemic. As professional sports franchises began to suspend their seasons, the Pegulas laid off all hospitality staff without any severance, healthcare, or guarantees of re-employment.

Despite being big Republican donors, the Pegulas have given generously to Cuomo, together donating $55,000 through two contributions in 2014.[54] Last year the couple treated Cuomo to a Bills game in the owner’s box.[55] Now Kim Pegula is a member of Cuomo’s re-opening advisory board.

The Jacobs family

Net worth: $3.8 billion

Wealth increase during pandemic: $600 million

Jeremy Jacobs Sr. is the billionaire founder and Chairman of Delaware North, a private, family-run, multibillion dollar concessions conglomerate. As the severity of the pandemic was beginning to unfold in March, the Jacobs family decided to place two-thirds of their company’s 3,100 full-time employees on temporary leave with only one single week of pay. Tens of thousands of part-time Delaware North employees were let go without any severance or support from the company or its billionaire owners.

From March 18 through May 15, the Jacobs family’s estimated net worth increased by $600 million, or 18.75%.

Jeremy Jacobs Sr and his wife Margaret are the largest donors in the family, together donating at least $117,000 to Cuomo from 2010 to 2014. In August 2014, Cuomo received matching $5,250 donations from each of Jeremy and Margaret Jacobs’ six children, as well as five of their children’s spouses, for a total infusion of $57,750 right before the democratic primary in New York in September.[56] On September 10, 2014, the day after he clinched the democratic nomination for Governor, Cuomo was feted with a fundraiser by Jeremy and Margaret Jacobs at their 250-acre estate in East Aurora, NY.[57] Cuomo’s Lieutenant Governor, Kathy Hochul, is married to Delaware North general counsel William Hochul.[58]

Now, despite their company’s reprehensible behavior and mass layoffs during the pandemic, Jeremy Jacobs Jr is serving on Cuomo’s re-opening advisory board and will have a say in the state’s strategy for addressing business interests as the pandemic continues to unfold.

The Jacobses are also major Trump supporters. After Trump was elected president in 2016, they held a fundraiser for his inauguration committee at the Delaware North corporate headquarters. Collectively, the family has given at least $167,700 to various Trump electoral committees – including his campaign committee, joint fundraising committee, and inauguration fundraising committee.[59]

-

https://www.rev.com/transcript-editor/shared/45n9TbLxQ1pnr1xmdDPZZbKcHak-yeE5m–K-2yYFtc9amWUTAkzGmPTLFrUZl0PwSocZV9WQeiDuBeox4gEc5TzJgc?loadFrom=PastedDeeplink&ts=3618.54 ↑

-

https://twitter.com/NYGovCuomo/status/1245021319646904320?s=20 ↑

-

https://dailygazette.com/article/2020/04/12/cuomo-returns-some-ventilators-to-niskayuna-nursing-home-donated-in-covid-19-effort ↑

-

https://thecity.nyc/2020/05/covid-hospital-case-rate-higher-in-areas-with-public-housing.html ↑

-

https://buffalonews.com/2020/05/10/covid-19-lays-bare-health-disparities-in-black-community-a-call-for-change-after-the-pandemic/ ↑

-

In a December 2019 analysis, we found that 49 billionaires have contributed to Cuomo: https://public-accountability.org/report/billionaires-have-fueled-andrew-cuomos-political-career/ ↑

-

https://www.governor.ny.gov/sites/governor.ny.gov/files/atoms/files/MEMBERS-OF-NEW-YORK-FORWARD-RE-OPENING-ADVISORY-BOARD.pdf ↑

-

Forbes “Billionaires 2020” list (with billionaire net worths as of March 18, 2020): https://www.forbes.com/billionaires/

Forbes “The World’s Real-Time Billionaires” list (billionaire net worth as of May 15, 2020 was used for this report): https://www.forbes.com/real-time-billionaires/#28b9b4053d78 ↑ -

IPS report: https://ips-dc.org/billionaire-bonanza-2020/

The IPS methodology and analysis showing US billionaire wealth increases in the early stages of the pandemic was fact-checked by USA Today: https://www.usatoday.com/story/news/factcheck/2020/05/07/fact-check-super-rich-got-richer-start-covid-19-pandemic/3069028001/ ↑ -

https://gothamist.com/news/cuomo-silent-taxing-ultrawealthy-while-pushing-billions-cuts-localities ↑

-

https://spectrumlocalnews.com/nys/central-ny/news/2020/03/20/medicaid-redesign-team-ii-recommends-hospital-cuts-amid-pandemic ↑

-

https://www.politico.com/states/new-york/albany/story/2020/03/27/cuomo-threatens-to-reject-67b-in-federal-aid-in-favor-of-medicaid-redesign-1269446 ↑

-

https://www.nydailynews.com/news/politics/ny-budget-cuomo-budget-details-20200402-57ifvc44vjeo3c4o57i6232vsy-story.html ↑

-

https://www.cityandstateny.com/articles/policy/budget/medicaid-cuts-make-state-budget-some-tweaks.html ↑

-

https://www.budget.ny.gov/pubs/archive/fy21/enac/fy21-enacted-fp.pdf ↑

-

https://www.budget.ny.gov/pubs/press/2020/fy21-enacted-fp-released.html ↑

-

https://www.census.gov/quickfacts/fact/table/NY,newyorkcitynewyork/PST045219? ↑

-

https://www.governor.ny.gov/sites/governor.ny.gov/files/atoms/files/EO_202.8.pdf ↑

-

https://ny.curbed.com/2020/3/30/21200066/coronavirus-new-york-rent-freeze-cuomo-covid-19 ↑

-

https://www.msn.com/en-us/lifestyle/pets/ny-gov-andrew-cuomo-my-daughters-have-stopped-paying-me-rent/vp-BB11YpDF ↑

-

https://www.governor.ny.gov/sites/governor.ny.gov/files/atoms/files/EO202.28.pdf ↑

-

http://rappcampaign.com/wp-content/uploads/COVID-May-13-media.pdf ↑

-

https://www.nydailynews.com/coronavirus/ny-coronavirus-prison-deaths-blacks-disproportionate-20200514-xjk4v5wowrhrfpiil5gevbgyui-story.html ↑

-

https://theintercept.com/2020/03/25/coronavirus-andrew-cuomo-new-york-bail-reform/ ↑

-

https://gothamist.com/news/ny-bail-reform-walk-back-stewart-cousins ↑

-

https://news.littlesis.org/2020/03/24/cuomo-puts-private-equity-vulture-in-charge-of-coronavirus-economic-recovery/ ↑

-

https://www.governor.ny.gov/sites/governor.ny.gov/files/atoms/files/MEMBERS-OF-NEW-YORK-FORWARD-RE-OPENING-ADVISORY-BOARD.pdf ↑

-

https://www.governor.ny.gov/news/amid-ongoing-covid-19-pandemic-governor-cuomo-and-mayor-mike-bloomberg-launch-nation-leading ↑

-

https://www.washingtonpost.com/education/2020/05/06/cuomo-questions-why-school-buildings-still-exist-says-new-york-will-work-with-bill-gates-reimagine-education/ ↑

-

https://www.syracuse.com/coronavirus/2020/05/former-google-ceo-to-lead-commission-to-reimagine-new-yorks-use-of-technology.html ↑

-

https://www.cbsnews.com/news/bill-ackman-billionaire-made-2-6-billion-coronavirus-meltdown/ ↑

-

https://www.cnbc.com/video/2020/03/18/watch-cnbcs-full-interview-with-billionaire-investor-bill-ackman-on-coronavirus-outbreak.html ↑

-

https://nypost.com/2020/03/23/coronavirus-outbreak-gooses-icahns-5b-bet-against-malls/ ↑

-

https://www.cnbc.com/2020/03/13/icahn-reveals-his-biggest-short-position-amid-market-turmoil-commercial-real-estate.html ↑

-

https://nypost.com/2020/04/07/hedgies-look-to-capitalize-on-hurting-firms-like-warren-buffett/ ↑

-

https://ciw-online.org/blog/2019/04/peltz-trian-pension-funds/ ↑

-

https://newsroom.regeneron.com/news-releases/news-release-details/regeneron-and-sanofi-begin-global-kevzarar-sarilumab-clinical ↑

-

https://www.forbes.com/sites/giacomotognini/2020/05/04/these-healthcare-billionaires-have-gotten-richer-off-the-coronavirus-pandemic/?fbclid=IwAR1IaT8kERz9iFxO0lLVYrqq8iPRZa4GiwZYw24WL51AZO4bi08j-C7EfrA#494f39e261ba ↑

-

https://www.lohud.com/story/money/personal-finance/taxes/tax-watch/2020/04/16/congress-candidate-adam-schleifer-net-worth/5138896002/ ↑

-

https://www.related.com/sites/default/files/2020-01/related-corporate-brochure_0.pdf ↑

-

https://www.cnbc.com/2020/04/06/related-companies-ceo-those-who-can-should-pay-their-rent.html ↑

-

https://www.vanityfair.com/news/2020/04/relateds-stephen-ross-trump-crony-has-a-giant-coronavirus-hypocrisy-problem ↑

-

https://cfapp.elections.ny.gov/ords/plsql_browser/CONTRIBUTORB_TYPE_CONTRIB ↑

-

https://cfapp.elections.ny.gov/ords/plsql_browser/CONTRIBUTORB_TYPE_CONTRIB ↑

-

https://www.washingtonpost.com/politics/trump-scheduled-to-headline-fundraisers-in-the-hamptons-where-tickets-run-as-high-as-250000/2019/08/06/47698530-b855-11e9-a091-6a96e67d9cce_story.html ↑

-

https://www.thedailybeast.com/trump-calls-for-re-opening-americas-gyms-day-after-call-with-soulcycles-owner ↑

-

https://cfapp.elections.ny.gov/ords/plsql_browser/CONTRIBUTORB_NAME ↑

-

https://www.facebook.com/news4buffalo/posts/kim-pegula-gov-andrew-cuomo-and-terry-pegula-watch-the-bills-game-from-the-owner/10157547403200505/ ↑

-

http://www.dailypublic.com/articles/11182014/power-public-money-grows-family-trees ↑

-

https://www.niagarafallsreporter.com/Stories/2014/NOV11/buff.html ↑

-

https://jcope.ny.gov/system/files/documents/2019/05/Kathleen%20Hochul%202018%20FDS.pdf ↑

-

http://www.dailypublic.com/articles/09052017/jeremy-jacobs-buffalos-billionaire-deportation-profiteer ↑