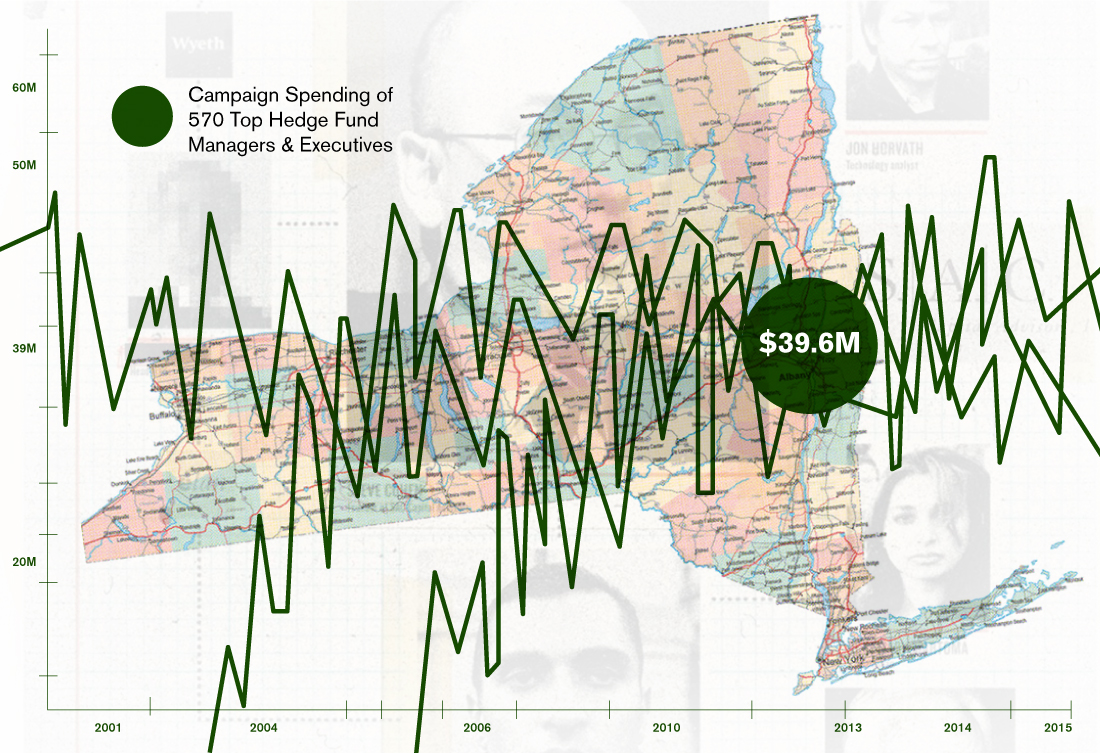

the Largest ever analysis of hedge fund influence in Albany shows that hedge funds & hedge fund managers spent $39.6 million in campaign cash

An analysis by Competitive Advantage Research, which examined the campaign spending of 570 hedge fund managers and senior executives over the past fifteen years, shows that hedge fund managers have exercised considerable influence over lawmakers in New York.

A thorough review of campaign finance records shows that 570 hedge fund managers and top executives have contributed $39,642,505.92 to more than 1,500 candidates and committees since 2000

We believe that this is the most comprehensive analysis of hedge fund campaign cash ever undertaken in New York.

The level of influence peddling from these hedge fund titans is staggering, especially when considering that the $39.6 million figure excludes lobbying and contributions to “dark money” organizations. » read more

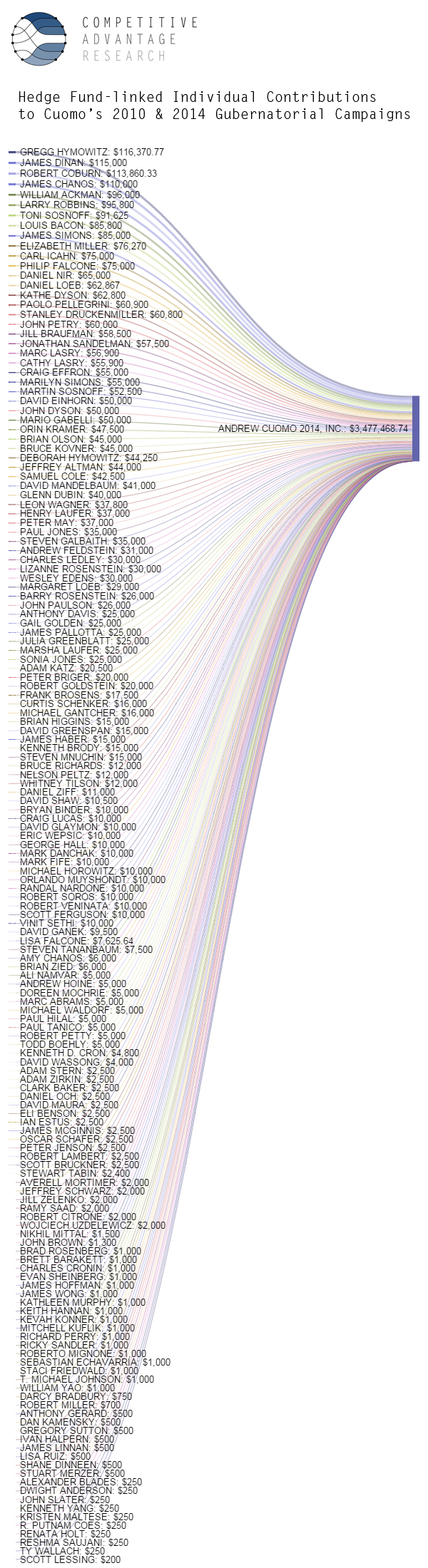

Topping the list of recipients is Gov. Andrew Cuomo, who raked in $4,832,140.34 over his tenure as Governor and Attorney General

In addition to this sum, hedge fund managers have spent $2.53 million filling the coffers of the New York State Democratic Party Committee’s Housekeeping fund, a Cuomo-controlled slush fund that has been used to pay for advertisements to support the Governor.[1]

Cuomo’s ties to the hedge fund industry are exceptionally troubling as his latest “ethics reform” proposal does not end the so-called “LLC loophole,” which allows wealthy individuals to easily circumvent maximum donation restrictions.[2]

As has been reported in Capital New York, Cuomo relies on a small network of very wealthy donors, who use the LLC loophole to bankroll his campaigns.[3] This loophole all but ensures that the power of the wealthy will always drown out the voices of millions of New Yorkers.

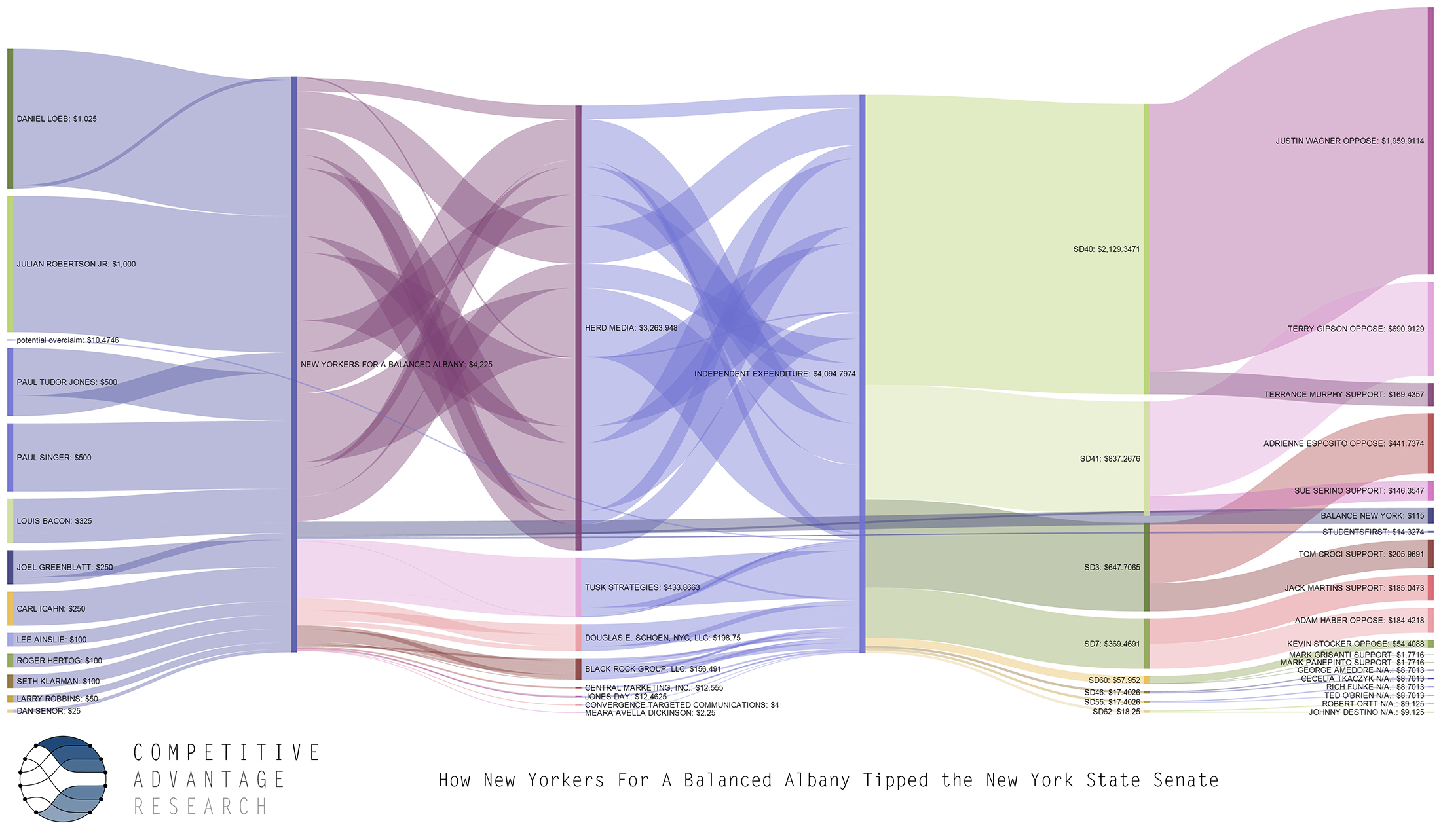

The second highest recipient of hedge fund largess was “New Yorkers for a Balanced Albany,” an independent expenditure committee backed by ten billionaires that helped flip the New York State Senate to Republican control in 2014.

While this group claims to support education reform, it appears to be little more than a shield to hide the influence of the billionaires. None of the $4.2 million in ads run by New Yorkers for a Balanced Albany dealt with education issues. Instead, several of the attack ads focused on undercutting public campaign financing, another campaign finance reform that would restrict the outsize influence of the wealthy in Albany.

Chart 1: Hedge fund contribution and spending through “New Yorkers for a Balanced Albany”—second largest recipient of hedge fund cash, after Governor Cuomo

Chart 2: Hedge fund contributions to Cuomo’s gubernatorial campaigns »

What the hedge fund managers bought: a New York tax structure that lets them pay lower tax rates than working people – and avoid some taxes altogether

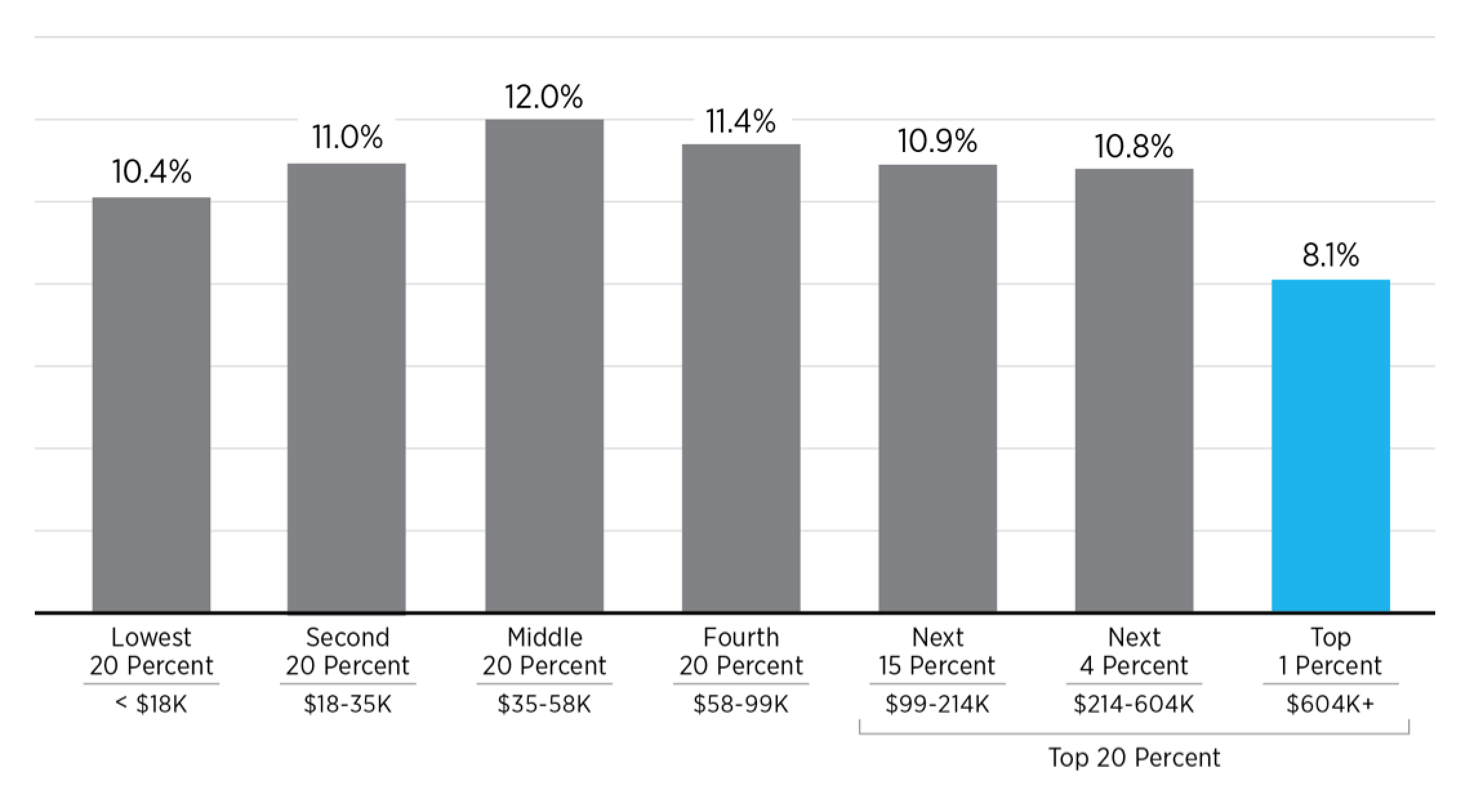

Hedge fund managers and billionaires in the richest one percent pay a smaller share of their income in combined state and local taxes than do lower- and middle-income families, according to a recent report from the Institute on Taxation and Economic Policy.[4]

The richest 1% of households in New York (those earning more than $600,000 per year) pays a tax rate of just 8.1 percent in state and local taxes.

The working poor pay a higher rate than the wealthy: New York households with incomes under $18,000 pay 10.4% of their income in state and local taxes.

The middle class pays a higher rate than the wealthy: New York households earning between $35,000 and $58,000 pay 12 percent of their income in state and local taxes.

As a result, some of the wealthiest hedge fund managers in New York are actually paying a smaller share of their income in taxes than their limousine drivers, dry cleaners, servants, helicopter pilots and doormen.

Chart: Percentage of State and Local Tax Burden by Income Group [5]

Chart: Percentage of State and Local Tax Burden by Income Group [5]

Here in New York, the wealthiest one-one hundredth of the top one percent (generally hedge fund managers, real estate barons and CEOs of large corporations) have average incomes of $69.6 million.

All that campaign cash has helped buy a state and local tax system that’s regressive — where the wealthy actually pay less than the poor and middle class, and nowhere near their fair share

New York’s state income tax applies a higher rate to the incomes of the rich, but it is not enough so to offset the effects of regressive sales and local property taxes.

In addition to benefitting from the general regressive structure of state and local taxes, hedge fund and private equity managers benefit from a number of specific elements of the tax code that benefit them, largely at the expense of the rest of us.

This preferential tax treatment has resulted in billions in lost revenue to the state of New York, and to reduced resources for essential public goods like education, infrastructure and mass transit.

The result: the wealthy and well-connected get big more tax breaks to allow them to grow even wealthier, and the middle class gets reduced services and higher taxes relative to income.

Hedge funds and hedge fund managers aren’t paying their fair share in taxes

Hedge funds and hedge fund managers use a number of specific loopholes in federal, state and local law to avoid taxes in New York.

Problem: Hedge funds use the “carried interest” loophole to avoid fair taxation.

By defining a large portion of their massive income as “carried interest,” hedge fund managers avoid fair-share taxes at the federal, state and local level in New York

Federal legislation to close the “carried interest” loophole is estimated to generate $17 billion dollars over ten years, an average of $1.7 billion per year.[6]

When a hedge fund manager invests capital provided by a limited partner, they typically take a share of the profits from that investment as a fee. That share is known as “carried interest.” This income should be subject to taxation, the same as any other income – but it isn’t.

Lost revenue under the loophole is largely the result of taxing personal income derived from carried interest at the difference between the federal capital gains rate and the top individual income tax rate — that difference is 19.6 percentage points.

Essentially, this is performance compensation – just like tips for a waiter or waitresses are performance compensation. But while a waitress is obliged to pay full income tax on this money, a hedge fund manager isn’t.

A new 19.6 percent surtax on carried interest, if adopted by all the states, would generate $1.7 billion per year. Each one percent of surtax would generate $89.5 million per annum nationwide. The Fiscal Policy Institute estimated in 2008 that 44% of the earnings of private equity occurred in New York City.[7]

If we assume that holds true today, then a 2.5 percent surtax applied to hedge fund income that is not being taxed appropriately at the federal level would generate $100 million per year for New York, repatriating lost revenue for use to fund schools and essential public services here.

Problem: Non-resident hedge fund managers are dodging New York State income taxes on much of their income

The 2010 Executive Budget proposal proposed to “expand the nonresident personal income tax to include income received from hedge fund management fees.” Currently, only a small portion of such income is taxed as compensation, with the remainder deemed tax-free capital gains. This proposal would result in equal treatment of this income for residents and nonresidents, and raise at least $50 million per year.

Problem: The “carried interest” loophole allows hedge funds to avoid many New York City business taxes

The City taxes a portion of the fees received by managing partners in private equity and hedge funds under its business tax system but exempts a portion known as “carried interest” from taxation.

When a fund manager invests capital provided by a limited partner, they typically take a share of the profits from that investment. That share is known as “carried interest,” and avoids City taxes.

Eliminating this loophole would put the taxation of private equity and hedge funds on the same footing as that of thousands of smaller businesses.

The New York City Independent Budget Office has estimated that eliminating the carried interest exemption from the New York City Unincorporated Business Tax would yield $200 million a year.[8]

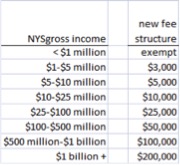

Problem: Hedge funds and luxury real estate developers use “LLCs” (limited liability corporations) to solicit huge investments, shield investors and limit taxation.

Some LLCs have huge amounts of New York State gross income — but they don’t pay their fair share in taxes and fees, unlike the small-to-medium sized businesses that anchor most communities.

From 2003 to 2006, New York instituted a fair-share LLC fee structure, which was later replaced with a flat-fee structure that allows hedge funds and speculative investment pools to avoid their fair share of the cost of public goods.

Since some LLCs have massive gross income, it would be fitting to apply roughly the same minimum taxes for other corporations (i.e. the 9A corporate tax) to the LLC fee structure.

The current 9A structure includes a fixed-dollar minimum corporate tax for businesses with gross income of $500M-$1B at $100,000, and for those with gross income > $1 B, the fixed dollar minimum tax is $200,000.

For 2015, DOB projects that the current LLC fee structure will generate $88 million. According to analysis by the Fiscal Policy Institute, a fair-share fee structure is projected to generate approximately $600 million, or roughly $500 million more than the existing fee structure.

For 2015, DOB projects that the current LLC fee structure will generate $88 million. According to analysis by the Fiscal Policy Institute, a fair-share fee structure is projected to generate approximately $600 million, or roughly $500 million more than the existing fee structure.

Problem: Cuomo eliminated the corporate minimum tax

The business tax “reform” package enacted by Governor Cuomo in 2014 will cost the state $440 million or more annually in reduced taxes when fully phased in.

Cuomo’s changes eliminated the capital base alternative tax (“corporate minimum tax”), which could result in some very large corporations paying a miniscule amount of tax relative to the volume of business they conduct in New York – possibly including hedge funds.

It should be restored and the cap increased to $25 million, to make sure big corporations doing business in New York pay at least some taxes.

Problem: Multi-millionaires and billionaires with huge yearly personal incomes are paying a smaller share of their income in state and local taxes than the middle class.

New York’s current “temporary” top income tax bracket is 8.82% for incomes of $2 million and over – and it is set to expire in 2017.

In 2010, there were about 3800 households filing taxes in New York with incomes at or over $10 million per year

A new 11% tax rate for this group would generate $1.7 billion per year in fair-share revenue for schools and services. Less than half (47%) of those affected are full-year New York State residents – many are hedge fund managers with homes all around the world

Instituting these new top rates would put the combined New York City and New York State top rate very close to the combined rate for California and San Francisco, leaving Silicon Valley wealth and hedge fund/Wall Street wealth comparably taxed.

Problem: Wall Street trading firms making billions in profit and getting taxpayer subsidies

Right now, investments in buildings and equipment used by broker/dealers are eligible for an investment tax credit. The credit is complex, subject to extensive recapture and concentrated among relatively few taxpayers, providing benefits to an extremely affluent and limited segment of the financial services industry.

For the last year for which data is available only 28 filers used this credit.[9]

This reform was recommended by the Solomon/McCall Tax Reform and Fairness Commission and was also proposed by Governor Cuomo in January 2014.[10]

Problem: Luxury Manhattan apartment owners from out of state or overseas that don’t live in their multi-million-dollar condos but still get special tax breaks

This reform gives pied-a-terre owners a choice: live full-time in your apartments and get tax breaks, or don’t live in them full-time and give up the breaks.

If each of the roughly 90,000 absentee-owner units in New York City were assigned a very modest average market value of $1.5 million each and a current tax assessment that – with 421a benefits, phase-in caps and improper assessments – equals about one-quarter of the real market value of the unit.[11]

With these assumptions, a 1.1 per cent tax rate on true market value would produce more than $900 million in new city revenues annually.

The Fiscal Policy Institute, using a similar analysis, has recommended that New York City introduce a graduated 4 percent tax based on comparable sales for all absentee-owner units with a market value of more than $5 million; that proposal, which would concentrate the tax burden on units worth more than $25 million, would bring in an estimated $250 million in new revenue every year.[12]

The state STAR program recently instituted a similar ban on tax breaks for second homes.

Fair-share revenue options would ensure hedge funds don’t dodge taxes and fully fund our public school system

Fair-share taxes and fees targeting hedge funds, billionaires, high-income LLCs and tax-dodging big corporations can raise between $3.1 and $4.2 billion dollars per year — more than enough to pay for complete compliance with the Campaign for Fiscal Equitss (“CFE”) decision, ensuring fair funding for all public schools.

Lawmakers should move forward with enough of the fair-share revenue options outlined in this report to ensure that this year’s state budget includes $2.2 billion in new school aid to comply with CFE and pay down Gap Elimination Adjustment arrears.

CLOSE HEDGE FUND TAX LOOPHOLES

- Repatriate New York State Share of Tax Revenue Lost to Federal Carried Interest Loophole: $100 million

- Tax Nonresident Hedge Fund Management Fees: $50 million

- Eliminate the Carried Interest Exemption under New York City’s Unincorporated Business Tax: $200 million

These initiatives close the “carried interest loophole” that lets hedge funds making billions in profits pay less in taxes than small businesses in our local communities, and assure that hedge fund managers working in New York but living elsewhere pay their fair share of taxes.

INSIST ON MINIMUM FAIR-SHARE TAXES FROM HEDGE FUNDS AND BIG CORPORATIONS

- Restore the Capital Base Alternative Tax (“Corporate Minimum Tax”) to the Corporate Franchise Tax: $500-$700 million

- Update LLC filing fees (applies to LLCs & non-LLC partnerships): $500 million

- Repeal the Financial Services Investment Tax Credit: $30 million

These initiatives assure that high-income LLCs, Wall Street and big businesses pay their fair share, while protecting local small businesses in our communities.

ENSURE THE SUPER-RICH PAY THEIR FAIR SHARE

- New top brackets on Personal Income Tax (PIT) 11% at $10M: up to $1.7 billion

- Close the Pied-a-terre Tax Abatement Loophole: $250-$900 million

- Helicopter Commuter Tax: $10 million

These initiatives ensure that billionaires and multi-millionaires pay their fair share of taxes, and close property tax loopholes benefitting the absentee owners of luxury Manhattan condominiums.

Cuomo’s debt to public school students perpetuates record-setting inequality

Data from the State Education Department shows that public schools in New York State are owed $5.9 billion in Foundation Aid and Gap Elimination Adjustment funding. These public schools have been chronically underfunded for years, as the state’s highest court found in the Campaign for Fiscal Equity (CFE) ruling.

Now, more than twenty years since the CFE lawsuit was filed and ten years since the final decision was delivered by the Court of Appeals, the state is still neglecting its constitutional obligation to provide a “sound basic education” for all New York City students.

Under Governor Andrew Cuomo, New York state government has failed to live up to the CFE ruling, continuing to underfund public schools and stubbornly refusing to pay what the courts have said is owed to them

This year’s state budget must include $2.2 billion in new school aid to comply with CFE and pay down GEA arrears.[13]

Governor Andrew Cuomo has failed to live up to his constitutional obligations to New York State’s school children. Governor Cuomo has consistently failed in his obligation to provide the resources necessary for all New York City students to receive the “sound basic education” that is guaranteed by New York State’s constitution.

Governor Cuomo is delinquent in the amount of $5.9 billion, owed to the New York State schools as a result of the Campaign for Fiscal Equity.[14]

Governor Cuomo has ignored CFE altogether despite promising to fund it when he ran for Governor in 2010. In his entire tenure he has never once proposed an increase in the Foundation Aid funding which is required in order to fulfill CFE.

Every Senate and Assembly District is owed tens of millions of dollars in funding for their schools in order for the state to fulfill its constitutional obligations to provide a “sound basic education.” The state’s funding delinquency affects every neighborhood in every school district.

As a result of underfunding, students are being shortchanged as schools have inadequate supplies, overcrowded classrooms, insufficient numbers of guidance counselors and social workers, understaffed and under resourced libraries, underfunded arts and sports programs, lack of sufficient tutoring and other supports for struggling students and reduced curriculum offerings and after school options.

These classroom cuts have the greatest negative impact on students in high-needs schools with large concentrations of students in poverty, students with disabilities and English language learners.

Fair-share taxes and fees targeting hedge funds, billionaires, high-income LLCs and tax-dodging big corporations can raise between $3.1 and $4.2 billion dollars per year – more than enough to pay for complete compliance with the Campaign for Fiscal Equity (“CFE”) decision and paying back the GEA arrears, ensuring fair funding for all public schools.

APPENDIX

FOOTNOTES

[1] http://blog.timesunion.com/capitol/archives/187527/common-cause-decries-soft-money-housekeeping-slush-funds/

[2] http://www.propublica.org/article/cuomo-has-raised-millions-through-loophole-he-pledged-to-close

[3] http://www.capitalnewyork.com/article/albany/2014/12/8558028/how-cuomo-raised-big-money-small-number-donors

[4] http://www.itep.org/whopays/

[5] Source: Institute on Taxation and Economic Policy (ITEP), January 2015

[6] http://ctj.org/ctjreports/2014/07/addressing_the_need_for_more_federal_revenue.php

[7] http://www.fiscalpolicy.org/FPI_RethinkingTaxTreatmentOfCarriedInterest.pdf

[8] http://www.ibo.nyc.ny.us/iboreports/options2013.pdf

[9] http://www.capitalnewyork.com/sites/default/files/131115__Incentive_Study_Final_0.pdf

[10] http://www.capitalnewyork.com/sites/default/files/131115__Incentive_Study_Final_0.pdf

[11] http://fiscalpolicy.org/fpi-proposes-tax-on-most-expensive-nyc-pied-a-terre-residential-units

[12] http://fiscalpolicy.org/fpi-proposes-tax-on-most-expensive-nyc-pied-a-terre-residential-units

[13] http://www.aqeny.org/wp-content/uploads/2015/02/legislative-prioririties-final.pdf

[14] http://www.aqeny.org/wp-content/uploads/2014/08/REPORT-NY-Billions-Behind.pdf