The Harmful Role of Hedge Funds in University Endowments

The Harmful Role of Hedge Funds in University Endowments

University endowments play an important role in the lives of students, faculty and other campus workers. Endowments are funded by donations, and universities use the investment returns to pay for improvements to buildings and facilities, provide scholarships, fund teaching and learning, and provide other services and economic support to the surrounding community.

Over the last decade, however, a troubling trend has emerged: Hedge funds—largely unregulated, high-cost investment vehicles run by the ultrawealthy—are managing larger and larger portions of these endowments, and charging universities the highest fees in the business to do so.

In 2015, over $100 billion of the more than $500 billion in U.S. university endowments was invested in hedge funds.[1]

Despite their popularity, hedge funds have done a great deal to endanger endowments and weaken higher education in the United States. They charge astronomically high fees, while delivering poor returns, and engage in dangerous practices that increase the personal wealth of hedge fund managers while making college more expensive and four-year degrees less attainable for all but the very rich.

In 2015, over $100 billion of the more than $500 billion in US university endowments was invested in hedge funds Share on X

This is the first major report to examine how hedge fund managers endanger endowments and harm students, faculty and staff in the process; in it, we expose how hedge funds contribute to and benefit from the defunding of higher education. from the defunding of higher education.

Key Findings: How Hedge Funds Undermine the Financial Health of Universities

Based on a careful review of the latest data and evidence, our analysis shows that many universities are cash-strapped because they have prioritized paying high fees to hedge fund managers while asking students, faculty and staff to make up the difference.

Many universities are cash-strapped bc they've prioritized paying high fees to hedge fund managers Share on X

Universities now face a choice: either continue to reward hedge fund billionaires who are set on siphoning money out of the higher education system, or divest from hedge funds entirely.

Here are the key findings of this report:

- Hedge funds collect billions of dollars in fees each year from U.S. colleges and universities—and produce little in return.

Our analysis suggests that hedge funds collected an estimated $2.5 billion in fees from university endowments in 2015 alone,[2] even though 2015 was reportedly the worst year for hedge fund performance since the financial crisis.[3]In fact, we estimate that from 2009-2015, university endowments paid an unbelievable $16.7 billion in hedge fund fees; when compared to returns, we estimate that endowments paid 60 cents in fees to hedge fund managers for every dollar of return on hedge fund investments to the endowment over this period.[4]

-

Hedge fund managers take up a disproportionate share of seats on college and university boards, influencing the endowments to make larger and riskier allocations to hedge funds.

The average university endowment has nearly 20 percent of its pool allocated to hedge funds,[5] and some universities now have upward of 40 percent of funds in this single asset class—a highly risky investment strategy that appears to benefit only hedge funds, not endowments.

University endowments paid an unbelievable $16.7 billion in hedge fund fees from 2009-2015 Share on X

- To bolster their public images as philanthropists, hedge fund managers make large, tax-free donations to private endowments, placing a huge burden on taxpayers—and driving inequality within the higher education system.

Hedge fund managers often make headlines for giving large sums of money to university endowments—yet these donations are almost exclusively aimed at rich Ivy League schools, not the public institutions that serve the majority of low- and middle-income students. And because these donations are untaxed, hedge funds save millions while taxpayers are left to pick up the tab.

-

Hedge funds invest endowment funds in an array of harmful industries—and use the investment gains to further a political agenda that harms students and communities.

Hedge funds have a pattern of investing endowment funds in problematic companies and industries that destabilize communities and environments across the globe—ranging from fossil fuels, private prisons and pharmaceuticals to foreclosed homes, student debt and for-profit universities.

By divesting from hedge funds, U.S. colleges and universities not only will save billions of dollars every year in hedge fund fees and lost returns, but also will dampen the undue influence that hedge fund managers have exerted over higher education in the U.S.

Universities can use these savings to keep tuition costs down, provide scholarships for middle- and low-income students, maintain a stable faculty workforce, pay campus workers a living wage, and fulfill their mission to serve as an economic anchor for the community.

Divesting from hedge funds, would save US colleges & universities billions every year in hedge fund fees and lost returns Share on X

According to recent figures, U.S. student loan debt has soared to $1.2 trillion,[6] and tuition has increased by nearly a third since 2008.[7] Meanwhile, universities are cutting the supports that make student success possible and replacing sustainable faculty positions with adjunct gigs; and wages for faculty, staff and campus workers have remained flat or in decline since the 1960s.[8] Public universities are now spending 23 percent less per student than they did pre-recession,[9] and students now contribute more out of pocket for a public college education than states do.[10] Even the wealthiest university, Harvard, whose endowment is valued at $38 billion,[11] last year paid less than half of its agreed-upon payments to the city of Boston in exchange for its use of city services.[12]

Behind the Numbers: A Closer Look at How Hedge Funds Profit from Endowments

In November 2015, the Roosevelt Institute and the American Federation of Teachers released a report, “All That Glitters Is Not Gold: An Analysis of U.S. Public Pension Investments in Hedge Funds,” which found that U.S. public pension funds are paying on average 57 cents to hedge fund managers for every dollar of investment return.

Here we use a similar methodology[13] to calculate that hedge funds received an estimated $2.5 billion in fees from university endowments in 2015 alone,[14] even though 2015 was reportedly the worst year for hedge fund performance since the financial crisis.[15]

Additionally, we estimate that, from 2009-2015, university endowments paid an unbelievable $16.7 billion in hedge fund fees; when compared to returns, we estimate that endowments paid 60 cents in fees to hedge fund managers for every dollar of return to the endowment over this period.[16]

Notably, this ratio of fees captured to net returns to investors is even higher than that of pension funds.[17]

How do hedge funds manage to collect such hefty fees, even in a record low performance year like 2015? Share on X

How do hedge funds manage to collect such hefty fees, even in a record low-performance year like 2015? The answer lies in the “two and twenty” fee structure that is typical of hedge funds, which means that investors must pay a management fee of 2 percent, and then a performance fee of 20 percent on any returns above a set target.[18] Even if an individual endowment fund is able to negotiate these fees down a little, they still dramatically outpace fees for every other kind of investment.

Compounding the issue of high fees and low returns for university endowment hedge fund programs is the failure of most universities to make a detailed accounting of hedge fund fees and returns available to the public.

In fact, it is not uncommon for universities to waive their right to know this information themselves. This prevents the board of trustees, students and other stakeholders from knowing the true cost of hedge funds to the university.

Following the Money: The Financialization of University Endowments

If hedge funds on the whole charge endowments disproportionately high fees for lackluster returns, why do endowments continue to invest hundreds of millions of dollars in hedge funds?

One reason may have to do with huge losses suffered by many endowments during the 2008-09 Great Recession—an economic crisis that, ironically, hedge funds played a significant role in creating.[19]

From July 1, 2007, through Dec. 1, 2008, the average endowment lost more than 25 percent of its value.[20]

Desperate to recoup losses, universities increased investment allocations to hedge funds, which made big promises Share on X

Endowments also may owe their ever-growing hedge fund allocations to the dramatic increase of hedge fund managers and other finance sector executives on their boards.

According to law professor Garry W. Jenkins in his 2015 article “The Wall Street Takeover of Nonprofit Boards”:

“Over the past twenty-five years the composition of the boards at some of America’s most important nonprofit organizations has dramatically changed. Without much notice, a legion of Wall Street executives (investment bankers, hedge fund managers, and others) has taken a growing number of seats in nonprofit boardrooms.”[21]

These nonprofit boardrooms include university endowments, where the “takeover” has been particularly evident.

According to Jenkins’ analysis, research universities and liberal arts colleges have seen the percentage of board seats held by finance industry professionals nearly double over the last 25 years. This trend is even more pronounced when it comes to board leadership: Currently, 56 percent of board leadership positions at research universities and 44 percent of board leadership positions at liberal arts colleges come from the financial sector.[22]

The disproportionate number of finance industry executives on university boards presents a number of problems, as Jenkins outlines in his critique, such as contributing to a lack of diversity on endowment boards, and bringing a finance industry approach to managing the endowment, with an emphasis on seeking higher short-term returns that may not square with the university’s mission.[23]

Additionally, our analysis suggests that the increased hedge fund presence on university boards is linked to many endowments’ riskily high hedge fund allocations.

The average endowment has about 20 percent of its assets invested in hedge funds.[24] This is more than double the allocation of the average pension fund (and pension funds, notably, do not have hedge fund managers serving on their boards).[25]

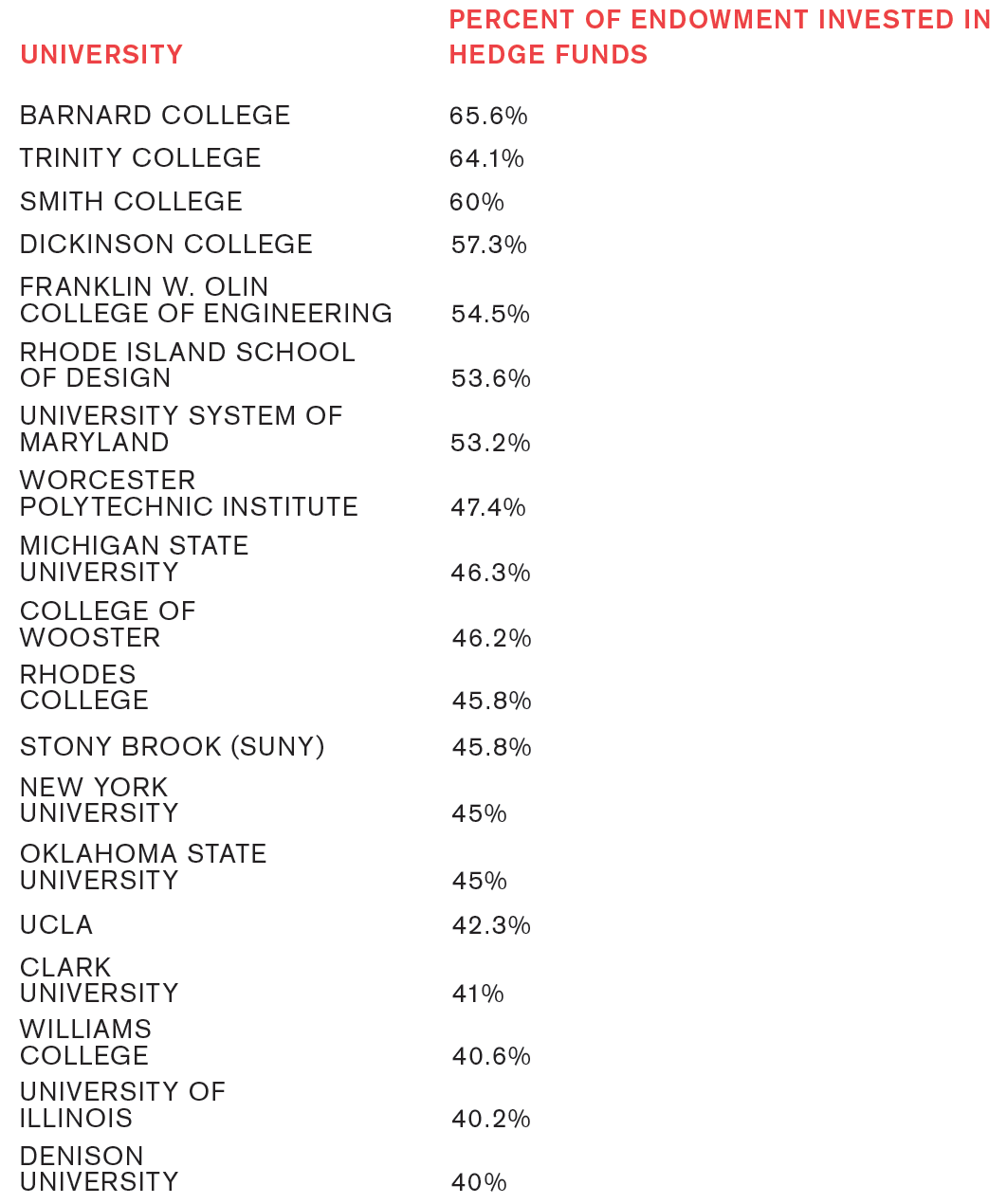

However, among those university endowments that currently invest in hedge funds, there is a group of endowments whose allocation to hedge funds exceeds 40 percent, an investment decision that is questionable at best.

Universities with 40 percent or more allocation to hedge funds:[26]

To put such a high percentage of an endowment fund in a single high-risk investment strategy like hedge funds makes little investment sense, especially if the goal is to diversify the fund and protect against downside loss.

Putting a high % of endowments in hedge funds is high cost & risk for schools. But lucrative for hedge fund mgrs Share on X

Considering this, it is perhaps not surprising that Barnard, which tops the list with nearly two-thirds of its endowment in hedge funds, has at least four current or former hedge fund managers, along with numerous other finance industry executives, serving on the board of trustees.[27]

New York University has a similarly financialized board, with at least six hedge fund managers, along with at least six private equity managers and a handful of other finance industry executives and attorneys representing hedge funds.[28]

Connecting the Dots: Hedge Funds, Inequality and University Endowments

In addition to their increased and troubling presence on endowment boards, hedge fund managers also influence our system of higher education by making massive donations to university endowments—usually to the Ivy League institutions where they received their degrees.

According to economist Robert Reich, the ballooning of elite university endowments happened in tandem with rapidly increasing income inequality in the U.S., with the relatively few extremely rich “donating [their millions] to causes they believe in, such as the elite private universities that educated them or that they want their children to attend.”[29]

This is welcome news for the few schools that cater to the affluent—such as Harvard and Yale—but it is little comfort to the low and middle-income students who struggle to pay for tuition at these schools.

Univ endowments spent nearly $3 on hedge fund & private equity fees for every $1 spent on scholarships Share on X

For example, according to a study of five large university endowments by law professor Victor Fleischer, the endowments spent nearly $3 on hedge fund and private equity fees for every $1 spent on scholarships.[30] Although some of these universities may claim that they offer free tuition to students from low- and moderate-income families, in practice it is difficult for many of these students, particularly first-generation college students, to know about and plan to take advantage of this assistance.

Hedge fund donations to elite institutions also disadvantage public universities and smaller schools because, as Reich contends, “a tax deduction is the same as government spending. It has to be made up by other taxpayers.”[31] Essentially, the tax-exempt status of these donations makes them a de facto government subsidy to wealthy, private institutions.

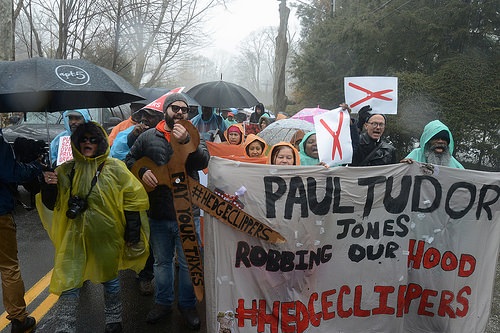

A good example of how this dynamic works is the recent $400 million donation to Harvard by hedge fund manager John Paulson in 2015, which represented the single largest donation the school had ever received.

Hedge fund donations to university endowments = a charitable donation tax exemption. Paulson saved ~$133 million Share on X

Because the gift qualifies for a charitable donation tax exemption, Paulson personally saved approximately $133 million[32] on this donation—which means that taxpayers were left to deal with the $133 million revenue hole left by his tax break. In other words, taxpayers ended up giving an additional $133 million to Harvard, the richest university in the country by far.

Adding to the problem is the fact that many hedge fund managers who donate to university endowments also manage endowment funds at other universities.

Paulson manages investments for UCLA and Texas Christian University[33] (in addition to sitting on the board of NYU).[34] Similarly, Seth Klarman of hedge fund Baupost Group made the naming donation to Harvard’s new conference center in 2014[35]—and also manages investments from Clark University, Cornell, UC San Francisco, the University of Texas, University of Washington and even Harvard itself.[36]

This arrangement in which Klarman both donates to the endowment and manages endowment funds is ethically questionable at best: Klarman’s donation was tax-exempt, but returns generated on his donation could result in income for him.

A recent study by the Nexus Research and Policy Center entitled “Rich Schools, Poor Students” quantifies these de facto subsidies, finding that, for example, Princeton University in New Jersey receives $105,000 per student, compared with the public Rutgers University (also in New Jersey), which receives only $12,000 per student.[37]

Some describe Harvard as a “hedge fund concern that happens to have a college attached” for tax purposes Share on X

Another study found that the 10 richest private universities have 16 times more endowment dollars to spend on students annually than do the 10 richest public universities.[38]

This has led some analysts to conclude that Ivy League schools such as Yale and Harvard would be better described as public institutions,[39] and some go so far as to describe Harvard as a “hedge fund concern that happens to have a college attached” for tax purposes.[40]

When university endowments hand over millions of dollars each year to wealthy hedge fund managers, they have less money available to spend on teaching and learning, a mission that is the basis of their tax-exempt status. ever received.

As Fleischer explained to USA Today, “The endowment is there to serve students in the present and in the future. But if the endowment accumulates too much, it’s really just serving the people who manage the money. That’s unethical, and it’s not consistent with why we allow endowments to be tax-exempt.”[41]

HEDGE FUNDS INVESTING IN BAD COMPANIES

An additional problem with hedge funds managing endowment assets has to do with the many problematic ways that hedge funds make money in the first place, and how they use their wealth to influence policy and politics in ways that undermine higher education, students and communities.

It has been well documented that many hedge funds invest endowment money in companies that harm communities across the globe.

Earlier Hedge Clippers reports analyzed how hedge funds prey on vulnerable communities from Puerto Rico to Baltimore, and enrich themselves by driving up the price tags of lifesaving pharmaceuticals and paying workers poverty wages. Later reports in this series will examine in-depth how hedge funds make billions through questionable investments in fossil fuels, private prisons, foreclosed homes, student debt and for-profit universities.

Likewise, over the past year, Hedge Clippers has exposed the schemes that ultrarich hedge fund managers use to influence government and tax policy to expand their wealth, influence and power.

Previous Hedge Clippers reports have highlighted how hedge fund managers influenced the outcomes of the New York gubernatorial election in 2014 and the Chicago mayoral election in 2015.

In each case, hedge fund managers succeeded in spending millions to elect a leader who then supported their pet causes of school privatization and tax breaks for the wealthy. (In the case of New York, the hedge fund managers even received proposed tax breaks on private jets and yachts in return for their support.)[42]

The following are just a few examples of hedge fund managers who use university endowment cash to invest in companies—and politicians—that do real harm to communities across the globe:

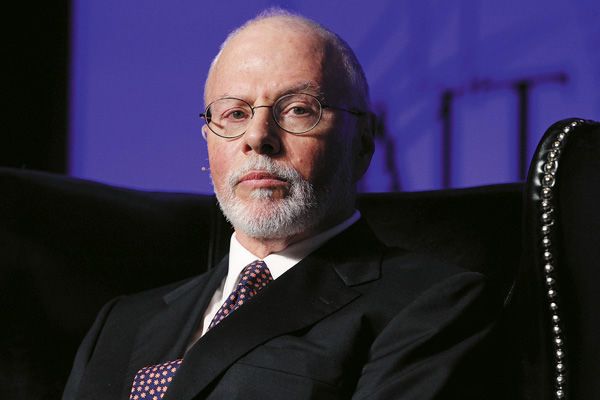

Paul Singer, Elliot Management

Paul Singer, founder of hedge fund Elliott Management, is one of the 400 richest Americans, with a personal net worth of $2.1 billion.[43] Singer amassed much of his fortune by, as a recent HedgeClippers paper described it, “doing something that most people couldn’t stomach—suing some of the poorest nations in the world,” including Argentina and the Congo.[44]

Singer was among the top 20 political donors during the 2012 federal election cycle, giving over $3.7 million of his personal wealth to Republicans and conservative causes.[45]

Elliott Management currently has large stakes in fossil fuel company Alcoa and Allergan pharmaceuticals, as of the company’s most recent SEC 13-F filings.[46]

Singer’s hedge fund manages endowment money for Michigan State University, Oregon State University, St. Olaf College, University of Rochester, Washington State University and Western Michigan University.[47]

Seth klarman, baupost group

Seth Klarman, CEO and president of the hedge fund Baupost Group, has a net worth of nearly $1.5 billion.[48] His hedge fund currently has holdings in Ocwen Financial,[49] which in 2013 settled with the Consumer Financial Protection Bureau for $2.2 billion over allegations that it “violated federal consumer financial laws at every stage of the mortgage servicing process,” and provided false or misleading information to consumers about the foreclosure process.[50]

Baupost has stakes in multiple fossil fuel companies, including Alcoa and Kosmos Energy, which does oil and gas exploration in Africa and South America.[51]

Baupost manages endowment money for Clark University, Cornell, Harvard (to which he also donates millions), UC San Francisco, University of Colorado, the University of Texas and University of Washington.[52]

John paulson, paulson & co.

John Paulson, founder of hedge fund Paulson & Co., is the 41st richest American, with an estimated net worth of $11.4 billion.[53]A significant portion of his personal wealth came from playing a leading role in the financial collapse of 2008.

In fact, Paulson was responsible for persuading Goldman Sachs and other large banks to create collateralized debt obligations (CDOs) for subprime loans, so that his company could bet against their value. Paulson & Co. then made $15 billion—with $4 billion going to Paulson personally[54]—by betting against U.S. homeowners.

Paulson recently has been described as embarking on a “spending spree”[55] in Puerto Rico, in an attempt to profit from the island’s economic crisis. Additionally, Paulson & Co. has holdings in HCA, the largest U.S. for-profit healthcare chain, which, in 2015 paid $15 million to the federal government to settle claims that the hospital chain was performing unnecessary heart surgeries in a Medicare fraud scheme.[56] Paulson also has holdings in Valeant Pharmaceuticals, which is currently under scrutiny for what some allege to be massive “Enron-like” fraudulent practices.[57]

Paulson was a top donor in the 2012 federal election cycle, contributing more than $1.2 million, all to Republicans and conservatives,[58] and reportedly financing the 2012 Republican National Convention with a $1 million donation.[59]

Paulson & Co. manages funds for Regents of the University of California, Texas Christian University and UCLA.[60]

Jeffrey Tannenbaum, Fir Tree Partners

Fir Tree Partners is one of the principal firms involved in Puerto Rico debt trade, and is believed to be the leader of a group of hedge funds buying up the island’s debt.[61] This group recently recommended that Puerto Rico lower its minimum wage, close schools and privatize public utilities in order to prioritize paying hedge fund billionaires for their debt holdings.[62]

Fir Tree is not new to this tactic of preying on vulnerable economies: It reportedly made 20 percent annualized returns as a holdout creditor in the Argentinian debt crisis, and was also active in purchasing Greek debt in recent years.[63] Like Paulson & Co, Fir Tree has holdings in HCA and Valeant; recent SEC filings also indicate that Fir Tree is invested in Monsanto.[64]

Fir Tree manages endowment money for Clemson University, Lewis & Clark College, Michigan State University, Oregon State, Southern Illinois University, Texas Tech, University of North Carolina at Greensboro, University of South Carolina, University of Vermont and Washington State University.[65]

Recommendations for Reform: How Endowments Can Limit the Harmful Impact of Hedge Funds

It’s clear that hedge funds consider university endowments to be a reliable source for easy money, collecting what we estimate to be 60 cents for every dollar of returns they give back to endowments—even when those returns are lower than other types of investments.

Over the years, hedge fund managers have worked their way onto university boards and donated large sums to elite schools, which has only increased their influence over how endowment funds are invested.

Even more disturbing is the fact that hedge fund managers use the billions of dollars in endowment funds to invest in companies that damage communities, and for political spending on politicians and policies that are in direct opposition to students, faculty and staff.

Top 25 hedge fund mgrs made $11.62b in 2014. Avg student now graduates with $35k worth of student debt. Share on X

The result has been hedge fund managers increasing their personal wealth and political power, while leaving students, faculty and staff to struggle with higher tuition costs, fewer scholarships, lower wages, benefit cuts and layoffs.

While the top 25 hedge fund managers made $11.62 billion in 2014,[66] the average student now graduates with $35,000 worth of student debt.[67]

Considering the destructive track record of hedge funds, colleges and universities should pursue the following reforms:

- Immediately divest from all hedge funds that have holdings in companies and industries that harm students, faculty and communities. Divestment should target companies and industries tied to fossil fuels, private prisons, student debt, gun manufacturers, payday lending, foreclosed homes and for-profit universities.

- Immediately perform a complete review of their hedge fund investments, including an analysis of past performance and fees paid, and a comparison with low-fee alternatives.

- Immediately make all hedge fund fee information available to the public online, and disclose a list of all hedge funds with which they have investments, along with any potential conflicts of interest.

- Advocate for state and federal legislation requiring full and public disclosure of all fees paid to hedge fund managers by all colleges and universities, public and private.

- Ensure that students’ and faculty members’ interests and views are adequately represented on boards of trustees and investment advisory board committees.

footnotes

[1] “2015 NACUBO-Commonfund Study of Endowments.” National Association of College and University Business Officers (NACUBO) and Commonfund Institute, released Jan. 27, 2016. http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[2] Based on the fee estimate methodology from “All That Glitters Is Not Gold,” which assumes a 1.8 percent management fee and an 18 percent performance fee on hedge fund investments. While many investors claim that they have negotiated fees down from the traditional “two and twenty” fee structure, our assumption is that in these cases investors have only negotiated fees down marginally. Additionally, many endowments utilize hedge fund-of-funds, which adds a significant layer of fees for the investor. Therefore, we believe that assuming a 1.8 percent and 18 percent fee structure is a conservative approach to estimating fees. “All That Glitters Is Not Gold” is available at: http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/. Data used to calculate these estimates obtained from the annual NACUBO-Commonfund Study of Endowments, years 2009-2015, available at: http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[3] See http://www.cnbc.com/2015/10/20/hedge-funds-see-worst-year-since-financial-crisis.html and http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/11917515/Hedge-funds-suffer-biggest-losses-since-the-financial-crisis.html.

[4] Based on the fee estimate methodology from “All That Glitters Is Not Gold,” available at: http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/. Data used to calculate these estimates obtained from the annual NACUBO-Commonfund Study of Endowments, years 2009-2015, available at: http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[5] Data obtained from Preqin, a database of alternative assets, including hedge funds. https://www.preqin.com/

[6] http://www.cnbc.com/2015/06/15/the-high-economic-and-social-costs-of-student-loan-debt.html

[7] http://money.cnn.com/2015/05/13/pf/college/public-university-tuition-increase/

[8] http://www.pewresearch.org/fact-tank/2014/10/09/for-most-workers-real-wages-have-barely-budged-for-decades/

[9] http://www.cbpp.org/research/states-are-still-funding-higher-education-below-pre-recession-levels

[10] https://www.washingtonpost.com/news/get-there/wp/2015/01/05/students-cover-more-of-their-public-university-tuition-now-than-state-governments/

[11] http://www.bloomberg.com/news/articles/2016-01-08/richest-u-s-schools-could-lose-tax-status-in-endowment-proposal

[12] https://www.bostonglobe.com/metro/2015/07/21/many-boston-colleges-fall-short-voluntary-payments-city/D8jVTjEKrPkMOZq8N4q83M/story.html

[13] Fee estimate methodology from “All That Glitters Is Not Gold,” available at: http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/. Data used to calculate these estimates obtained from the annual NACUBO-Commonfund Study of Endowments, years 2009-2015, available at: http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[14] Based on the fee estimate methodology from “All That Glitters Is Not Gold,” which assumes a 1.8 percent management fee and an 18 percent performance fee on hedge fund investments. While many investors claim that they have negotiated fees down from the traditional “2 and 20” fee structure, our assumption is that in these cases investors have only negotiated fees down marginally. Additionally, many endowments utilize hedge fund-of-funds, which adds a significant layer of fees for the investor. Therefore, we believe that assuming a 1.8 percent and 18 percent fee structure is a conservative approach to estimating fees. “All That Glitters Is Not Gold” is available at: http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/. Data used to calculate these estimates obtained from the annual NACUBO-Commonfund Study of Endowments, years 2009-2015, available at: http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[15] See http://www.cnbc.com/2015/10/20/hedge-funds-see-worst-year-since-financial-crisis.html and http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/11917515/Hedge-funds-suffer-biggest-losses-since-the-financial-crisis.html.

[16] Based on the fee estimate methodology from “All That Glitters Is Not Gold,” available at: http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/. Data used to calculate these estimates obtained from the annual NACUBO-Commonfund Study of Endowments, years 2009-2015, available at: http://www.nacubo.org/Research/NACUBO-Commonfund_Study_of_Endowments.html.

[17] http://rooseveltinstitute.org/all-glitters-not-gold-analysis-u-s-public-pension-investments-hedge-funds/

[18] “Two and Twenty,” Investopedia, www.investopedia.com/terms/t/two_and_twenty.asp.

[19] See http://www.ft.com/intl/cms/s/0/e83f9c52-6910-11e1-9931-00144feabdc0.html#axzz3x4HYjiIh

[20] http://www.usnews.com/education/articles/2009/01/27/the-recession-hits-college-campuses

[21]

http://ssir.org/articles/entry/the_wall_street_takeover_of_nonprofit_boards#sthash.KbzPmzix.dpuf

[22]

http://ssir.org/articles/entry/the_wall_street_takeover_of_nonprofit_boards#sthash.KbzPmzix.dpuf

[23] http://ssir.org/articles/entry/the_wall_street_takeover_of_nonprofit_boards

[24] Preqin. https://www.preqin.com/

[25] This may be due in part to the fact that most public pension plans are subject to rules requiring that board members represent stakeholders or representatives of those responsible for funding the plan, as well as independent directors.

[26] This list excludes universities with endowments of less than $300 million. All data obtained from Preqin and reflect records updated between Sept. 29, 2015, and Jan. 28, 2016, with the exception of Trinity College (data last updated March 2015), and Clark University (data last updated June 2015). https://www.preqin.com/

[27] http://barnard.edu/about/leadership/trustees

[28] https://www.nyu.edu/about/leadership-university-administration/board-of-trustees.html

[29] http://billmoyers.com/2014/10/17/government-spends-per-pupil-elite-private-universities-public-universities/

[30] http://college.usatoday.com/2015/09/03/yale-university-endowment/

[31] http://billmoyers.com/2014/10/17/government-spends-per-pupil-elite-private-universities-public-universities/

[32] Assuming a charitable donation tax break of about 33 percent.

[33] https://www.preqin.com/user/hf/FundManagers/HF_FundManagerGPProfile.aspx?FirmId=12819

[34] https://www.nyu.edu/about/leadership-university-administration/board-of-trustees.html

[35] http://harvardmagazine.com/2014/06/harvard-business-school-klarman-hall

[36] Preqin. https://www.preqin.com/user/hf/FundManagers/HF_FundManagerGPProfile.aspx?FirmId=20690

[37] http://www.chron.com/news/education/article/Study-reveals-private-schools-receiving-large-6184996.php

[38] http://higheredincrisis.org/2015/05/does-wealth-inequality-among-universities-pose-a-threat-to-the-american-economy-part-1/

[39] https://www.washingtonpost.com/news/grade-point/wp/2015/04/06/are-harvard-yale-and-stanford-really-public-universities/

[40] http://nymag.com/daily/intelligencer/2014/09/take-away-harvards-nonprofit-status.html

[41] http://college.usatoday.com/2015/09/03/yale-university-endowment/

[42] http://nypost.com/2015/03/31/new-york-state-giving-huge-tax-break-to-luxury-yacht-buyers/

[43] http://www.forbes.com/profile/paul-singer/

[44] https://hedgeclippers.org/1464797090949/paul-singer/

[45] https://www.opensecrets.org/bigpicture/topindivs.php

[46] http://www.sec.gov/Archives/edgar/data/1048445/000114036115041833/xslForm13F_X01/form13fInfoTable.xml

[47] https://www.preqin.com/user/hf/FundManagers/HF_FundManagerGPProfile.aspx?FirmId=7867

[48] http://www.forbes.com/profile/seth-klarman/

[49] http://www.sec.gov/Archives/edgar/data/1061768/000114036115041178/xslForm13F_X01/form13fInfoTable.xml

[50] http://dealbook.nytimes.com/2013/12/19/big-mortgage-servicer-reaches-settlement/?_r=0

[51] http://www.sec.gov/Archives/edgar/data/1061768/000114036115041178/xslForm13F_X01/form13fInfoTable.xml

[52] Preqin. https://www.preqin.com/

[53] http://www.forbes.com/profile/john-paulson/

[54] http://www.wsj.com/articles/SB10001424052748703574604574499740849179448

[55]

http://pagesix.com/2015/08/20/hedge-funder-john-paulson-goes-on-puerto-rico-spending-spree/

[56] http://www.modernhealthcare.com/article/20150928/NEWS/150929880

[57] http://money.cnn.com/2015/10/21/investing/valeant-enron-bill-ackman/

[58] https://www.opensecrets.org/bigpicture/topindivs.php

[59] https://www.opensecrets.org/news/2015/06/harvards-billionaire-benefactor-also-a-gop-sugar-daddy/

[60] https://www.preqin.com/user/hf/FundManagers/HF_FundManagerGPProfile.aspx?FirmId=12819

[61] https://hedgeclippers.org/1464797090949/hedgepapers-no-17-hedge-fund-billionaires-in-puerto-rico/

[62] http://www.theguardian.com/world/2015/jul/28/hedge-funds-puerto-rico-close-schools-fire-teachers-pay-us-back

[63] https://hedgeclippers.org/1464797090949/hedgepapers-no-20-new-york-citys-public-pension-vultures-in-puerto-rico/#_edn4

[64] http://www.sec.gov/Archives/edgar/data/1056491/000131586315000925/xslForm13F_X01/firtree3q15.inftab.xml

[65] https://www.preqin.com/user/hf/FundManagers/HF_FundManagerGPProfile.aspx?FirmId=14063

[66] http://www.institutionalinvestorsalpha.com/Article/3450284/The-2015-Rich-List-The-Highest-Earning-Hedge-Fund-Managers-of-the-Past-Year.html

[67] http://time.com/money/4168510/why-student-loan-crisis-is-worse-than-people-think/