UPDATE: Carlos García Fails to Report CommoLoCo in Financial Disclosure

García’s business makes small loans to desperate Puerto Ricans at extremely high interest rates

The following is an update concerning the business interests and apparent conflicts of Carlos García, who is serving as a board member of the Financial Oversight and Management Board for Puerto Rico (aka “Fiscal Control Board,” “Junta”).

- A report issued last December by the Committee for Better Banks and the Hedge Clippers, entitled “Pirates of the Caribbean” examined a web of conflicts between García’s former employer Santander Bank and the Government of Puerto Rico surrounding debt issuance, which has helped create a humanitarian crisis in Puerto Rico.

- The report places Carlos García at the center of these conflicts, because he served as a senior executive at Santander while the bank advised on debt deals and underwrote bonds for the Commonwealth. García left Santander to become head of Puerto Rico’s Government Development Bank, which under his leadership orchestrated a massive issuance of questionable public debt that was often underwritten by Santander

In order to comply with federal conflict of interests laws, the Fiscal Control Board for Puerto Rico members including Carlos García have published their personal financial disclosure reports.

Disclosure highlights more conflicts of interest for Carlos García

- Our investigation into his financial disclosure shows that García did not reveal the salaries he receives as Chairman of the privately held Caribbean Financial Group, Inc., which is based in Puerto Rico, or as the CEO of BayBoston Managers LLC, a private equity firm he established, which is located in Newton Center, Massachusetts.

- The financial disclosures have sparked criticism of several board members for failure to fully document their financial situation as required by the PROMESA law.[i] The leader of the Popular Democratic Party (PPD), Hector Ferrer, has called on Junta members Jose Carrion and Carlos García to disclose all the required information about their assets and income which wasn’t reported on their disclosure forms. Ferrer said that a failure to be transparent would “disqualify them as members of the fiscal control board.”[ii]

García also omitted from his disclosure any detailed description of the nature of his business interests in Puerto Rico. García discloses that he is the Chairman of the Caribbean Financial Group (“CFG”) but does not reveal that its business consists of making “unsecured personal loans and related credit insurance products to individuals who may have limited access to consumer credit from banks and other traditional lenders.” [iii] In Puerto Rico the trade name for this business is CommoLoCo, which makes small, unsecured personal loans, known as ‘prestamos personales’ in Spanish.

- On its website, commoloco.com, the company claims that an online personal loan applicant will receive a response within 30 seconds. On its homepage, CommoLoCo also provides an example of a personal $1,000 loan to be repaid in monthly installments of $33.16 over four years (a total of $1,592), which suggests an interest rate of 25% for the loan.

- However, a recent visit to a CommoLoCo storefront location, a potential consumer reported anecdotally learning that loans can carry interest rates of up to 49% — almost twice that amount. Puerto Rican law has no cap on interest rates for ‘prestamos personales,’ and the majority of these loans made in 2016 had interest rates between 31% and 43%.[iv]

- According to a case study published by IBM in 2016, the business of CFG is “booming.” The case study notes that “CFG has expanded rapidly – with year-on-year earnings growth exceeding 10 percent.”[v]

- García has a special stake in CFG’s business in the Commonwealth. He reveals in his disclosure that he is “eligible for a special bonus from CFG in case of the acquisition of a consumer finance business in Puerto Rico.” [vi] He does not disclose the name of the business, but his statement suggests that he will be handsomely rewarded by the expansion of CFG’s operations on the island.

- In addition, García has raised capital for the Caribbean Financial Group through his private equity company. A limited liability corporation known as BayBoston CFG Investors, which García manages, has filed a Form 4 with the U.S. Securities and Exchange Commission, reporting a sale of $3.65 million in equity securities.[vii] García notes in his disclosure that the purpose of BayBoston CFG Investors is to invest in the Caribbean Financial Group.[viii] The BayBoston website homepage currently lists Caribbean Financial Group Holdings, L.P. as an “active investment.”[ix]

Companies that make small, unsecured personal loans at interest rates as high as 31%, 43% or even potentially as high as 49% — to individuals with poor credit will likely profit from the desperation created by Puerto Rico’s humanitarian crisis. The crisis is fueled in part by Puerto Rico’s overwhelming debt burden, which García played a role in creating. Today, he is personally involved in directing and raising money for a predatory lender that targets Puerto Ricans, i.e. as the Chairman of CFG, through his private equity firm’s investment in the CFG, and the “special bonus” he may receive from its expansion.

Carlos García should resign

The work of the Junta is not compatible with the business of making loans at unlimited and exorbitant rates.

- García should resign immediately from the Fiscal Control Board. The outcome of the PROMESA mandated process will determine for thousands of Puerto Ricans whether they will enjoy access to traditional sources of consumer credit or whether they will be forced in desperation – through circumstances beyond their control – to rely on predatory lenders like CommoLoCo.

DOWNLOAD UPDATE HERE

Descárgate este informe en español aquí

EXECUTIVE SUMMARY

Former Santander executives José Ramon Gonzalez and Carlos M. Garcia served as heads of Puerto Rico’s Government Development Bank (GDB) and Santander[1] in Puerto Rico. Garcia and Gonzalez were recently appointed to 2 of the seven seats of the PROMESA Fiscal Control Board. Together, these men built Santander Securities, the bank’s municipal bond business, which established itself as a leading bond underwriter coinciding with the growth in Puerto Rican public debt. This business brought in substantial fee income for the bank.

Carlos M. Garcia was appointed to head the GDB in 2009 by Governor Luis Fortuño, who implemented an austerity plan when he took office in Puerto Rico, laying off tens of thousands of public employees, privatizing public assets, and attempting to provide economic stimulus through targeted tax cuts and public private partnerships.

Carlos M. Garcia established a team of current or former Santander executives to run the GDB between 2009 and 2012.

To run the GDB, Garcia established a team of current or former Santander executives that maintained its grip on the GDB throughout the Fortuño administration. In 2011, Garcia left the GDB to return to Santander, while Santander executive Juan Carlos Batlle moved to replace Carlos Garcia as the head of the GDB. At the same time, Juan Carlos’ brother Fernando Batlle left the GDB to become CEO of Santander Securities – creating a virtual revolving door of brothers.

As GDB President, Garcia moved swiftly to reassure the bond market and maintain Puerto Rico’s credit ratings by relying on a new category of municipal debt, secured by regressive Puerto Rican sales and use taxes. These “safe” bonds, known by their Spanish language acronym, COFINA, are “extra-constitutional,”[2] and were issued mainly as refinancing bonds, which diverted Puerto Ricans’ sales tax revenue to paying bondholders instead of funding public programs. Fortuño had a law passed in January 2009 that doubled the amount of sales tax revenue set aside for COFINA bonds, enabling Garcia’s GDB to issue more debt underwritten by Santander and other banks. Public Law 7, passed March 2009, permitted the Treasury Secretary to refinance debt without considering whether it would actually save Puerto Rico money.

José Ramon Gonzalez established Santander Securities, the bank’s municipal bond business, in Puerto Rico.

During the Fortuño years, as Puerto Rico fell deeper into debt and Santander and other banks elicited demand for Puerto Rico’s triple tax-exempt bonds, the GDB became increasingly reliant on questionable financial engineering techniques. Santander helped the Commonwealth issue risky debt deals that relied on controversial features such as capital appreciation bonds, capitalized interest, and interest rate swaps. These generated more fee income for Santander’s underwriting business.

In one case, Santander helped underwrite a bond issue in 2011 to raise money to pay a $400 million interest rate swap termination, which could have been used to fund healthcare or infrastructure. In another example, Santander and other banks earned at least $35.7 million in underwriting fees in three Employee Retirement System (ERS) debt deals worth $2.9 billion that used employers’ contributions as collateral, virtually unheard of for public pension funds. This debt added to the pension fund’s liability and it is forecasted to run out of money in two years.

The PROMESA Fiscal Control Board, colloquially known as “the Junta.”

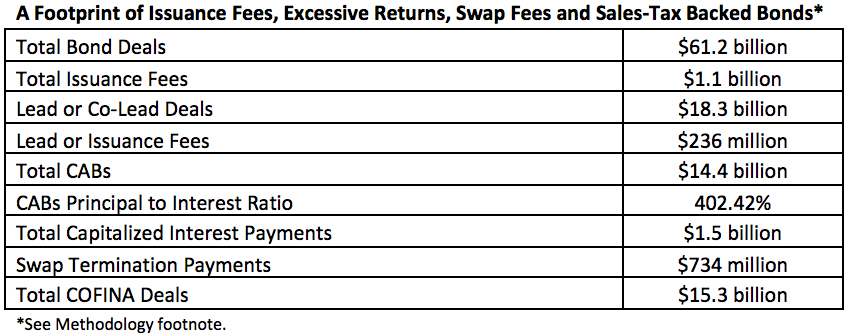

We examined 90 debt deals that Santander participated in underwriting, from general obligation bonds to the extra-constitutional COFINA bonds, to the GDB’s affiliates and subsidiaries. We found the total amount of the debt issued where Santander played an underwriting role to be $61.2 billion dollars—almost as much as the figure currently used as an estimate of the Commonwealth’s total outstanding debt load of more than $70 billion. More than $1 billion from these bond deals went to fees paid to Santander and other banks. We also examined Puerto Rican bond deals that Santander underwrote to see if they contained features such as CABs, capitalized interest, interest rate swaps, and whether the bonds were issued by special purpose entities.

As the U.S.’s largest unincorporated territory without legal authority to restructure its debt equal to other U.S. municipalities, Puerto Rico is facing both a fiscal catastrophe and an unprecedented humanitarian crisis. Wall Street saw the debt crisis as an opportunity, and yet bankers have been able to seize on it both as a business and policymaking opportunity. A key question all Puerto Ricans must ask – should banks like Santander be held accountable for their role in Puerto Rico’s debt crisis?

Puerto Rico’s ambiguous political situation and inability to restructure its debt has left it vulnerable to interlopers from Wall Street and banks.

For its role in advising the government and facilitating the issuance of questionable debt that led to a fiscal catastrophe, we call on Santander to refund all the underwriting fees and discounts it received from the Puerto Rican government. Much of this debt relied on controversial financial engineering, and was underwritten when the bank had conflicted relationships with the government. Second, José Ramon Gonzalez and Carlos Garcia should resign from the PROMESA Fiscal Control Board. As architects of the debt crisis, they should not be put in positions of power to adjudicate its outcome. Third, the Puerto Rico Commission for the Comprehensive Audit of the Public Credit (the Audit Commission) should continue to be funded and empowered to complete its investigation of the debt and its legitimacy, so that the Puerto Rican people are provided with real answers.

Introduction

Banks bear responsibility for exacerbating Puerto Rico’s debt crisis. Current analysis rightfully sheds light on the role of entities like hedge funds, but banks’ role in eliciting demand and understating risk[3] for the island’s tax free municipal bonds has been sorely neglected. Santander, an important bank operating in Puerto Rico since 1976, played a crucial role in structuring and profiting off Puerto Rican debt through a revolving door with Puerto Rico’s Government Development Bank (“GDB”).[4] Two former Santander executives, José Ramon Gonzalez and Carlos M. Garcia, served as heads of the GDB and Santander Securities, which advised Puerto Rico on municipal debt and underwrote many of its troubled bond offerings. Garcia went directly from Santander to the GDB and back again.

José Ramon Gonzalez and Carlos M. Garcia, served as heads of Puerto Rico’s GDB and Santander Securities, were recently appointed to the Junta.

In a striking irony, Garcia and Gonzalez, who helped devise and market the bonds that helped bring Puerto Rico to its knees, were recently appointed by U.S. politicians to 2 of the seven seats on the PROMESA Fiscal Control Board (colloquially known as “the Junta”). The Junta has broad powers to address the Puerto Rican debt crisis. It has authority to decide how to restructure Puerto Rico’s debt, which bondholders will be repaid and how much they will receive. In essence, the Junta has Puerto Rico’s future in its hands.

During the administration of Luis Fortuño, Puerto Rico’s governor from 2009 until 2012, Carlos Garcia and a group of former Santander executives were appointed to run the GDB and instituted a massive bond issuance program[5] that lies at the root of the solvency crisis facing Puerto Rico today. This group also facilitated the creation and distribution of bond deals that contained features such as capital appreciation bonds and interest rate swaps that some experts have termed “predatory” and which Santander profited from as an underwriter and broker-dealer.[6]

Carlos M. Garcia was appointed to Puerto Rico’s GDB in 2009.

Puerto Rico is the largest unincorporated territory in the U.S. subject to federal law, yet citizens lack full voting rights and democratic representation in Congress. Over a century, the U.S. has imposed tax policies on Puerto Rico that serve U.S. corporate interests first, like IRS Section 936, which provided a tax benefit to U.S. corporations, and was phased out over a ten-year period beginning in 1996. The dominant public narrative that usually portrays Puerto Rico as a dependent, irresponsible and costly stepchild to its generous mainland U.S. benefactor is dangerously shortsighted when applied to the island’s situation today. Puerto Rico’s ambiguous political status has made it vulnerable to the influence of interlopers from banks and Wall Street, as Congress has not given Puerto Rico legal authority equal to that of U.S. municipalities to restructure its debt. [7]

The U.S. has imposed tax policies on Puerto Rico that serve U.S. corporate interests first. Share on XWe estimate Santander has participated in the underwriting of $61 billion in Puerto Rican bonds, and as part of these bond issues, $1.1 billion was paid to Santander and others in issuance fees.

Because of its fiscal catastrophe, Puerto Rico now faces a humanitarian crisis. Almost half of Puerto Ricans live in poverty, 37% of children live in extreme poverty, and unemployment is over 12%.[8] Six hundred of the island’s 1,400 schools are expected to be closed in the next few years. Hospitals are struggling to staff operations and pay utility bills, and over a quarter of the population is expected to be infected with the Zika virus by the end of 2016.[9]

Puerto Rico is facing an unprecedented humanitarian crisis

As the urgency of this crisis grows, banks like Santander that facilitated and profited from its creation must step forward, accept responsibility and make financial amends to the people of Puerto Rico. The former Santander executives who were appointed to the Junta should resign because of their role in helping create the crisis and their conflicts of interest in setting policies to adjudicate disagreements between creditors about debt they helped manufacture.

This report is the first of three looking into Santander and its business enterprises in Puerto Rico, which profited off of the public debt that has caused such misfortune for the Puerto Rican people.

A bird’s eye view of Santander’s critical role in underwriting Puerto Rican debt

In our analysis of Puerto Rican public debt, we found at least 90 instances in which Santander participated in underwriting municipal bond issues, from general obligation bonds to the extra-constitutional COFINA bonds highlighted below, to the GDB’s affiliates or subsidiaries— including the electric utility, the public pension plan, the Employee Retirement System; and housing, hotel and tourism, sewer and aqueducts, public buildings, infrastructure financing and other Puerto Rican authorities.

Municipal debt underwriters purchase newly issued securities from the governmental issuer and then sell those securities to investors. They receive a discount on the bonds or a fee—called the issuance fee— from the government as compensation. They also work to structure municipal bond offerings and to determine their offering price.

We found the total amount of the debt issued in which Santander played an underwriting role, to be $61.2 billion dollars—almost as much as the figure currently used as an estimate of the Commonwealth’s total debt load of more than $70 billion.[10] More than $1 billion was diverted from these bond deals as issuance fees and for Santander and other banks underwriters’ discount, legal, printing, and other fees. Among the Puerto Rican bond issues in our analysis, Santander was a lead or joint lead underwriter of over $18.3 billion in debt issued, of which over $236 million in fees were put into the hands of Santander and other banks.

As Puerto Rico fell deeper into debt, municipal bond underwriters like Santander advised the Commonwealth on increasingly risky debt deals. Bond deals more often began to feature controversial financial engineering techniques, including capital appreciation bonds (CABs), capitalized interest, interest rate swap agreements, and special purpose entities that issued “extra-constitutional debt.[11]

We examined bond deals that Santander underwrote to see if they contained features such as CABs, capitalized interest, interest rate swaps, and whether the bonds were issued by special purpose entities.

Capital appreciation bonds are long-term bonds in which the borrower does not pay interest or principal until the bonds come due. As the bonds mature, interest is added and compounded, which results in an unusually large payout to the borrower. CABs are associated with municipal debt loads that some experts have labeled “abusive,” and recent legislation in California and Texas has restricted their use.[12] In most CABs, the amount borrowed is not to be paid back over a substantial period of time. Of the $61.2 billion in total debt reviewed, we found Santander participated in underwriting 20 deals that had CABs totaling $14.4 billion, 9 of which were COFINA deals.[13] In the cases where the bonds’ Official Statements reported the CABs’ worth at maturity and thus the future interest due, we found $2.3 billion in principal was borrowed with $10.2 billion in interest at maturity: an interest to principal ratio of 433%. By contrast, a traditional ten-year bond paying 5% simple interest on $10 million will yield $5 million in interest payments over the life of the bond, an interest to principal ratio of 50%.

While the child poverty rate in Puerto Rico is 37%, banks like Santander helped the Commonwealth issue increasingly risky debt deals.

Capitalized interest is borrowing in order to make interest payments – the profits due to bondholders. In Puerto Rico, bonds and refunding bonds were issued partly to cover interest payments, which turned older debts’ interest into new principal, increasing the amount owed.[14] In our analysis, we found a third of Santander-underwritten deals contained capitalized interest payments totaling $1.5 billion of payments that are essentially interest on interest.[15]

Swap termination payments are fees paid to banks or other Wall Street firms to cancel interest rate swaps. Interest rate swaps are periodic exchanges of money between holders of fixed-rate and variable-rate debt. The exchange amount is based on an agreed-upon notional amount and movement of interest rates.[16] Although these swaps were meant to lower Puerto Rico’s borrowing costs if interest rates rose, they were, in fact, sometimes costlier for the government as interest rates remained near record lows.[17] When bonds were downgraded by rating agencies, some of the swaps accelerated to default rates at a high cost to Puerto Rico.[18] Of the 90 bonds we examined in which Santander was a lead or participating underwriter, we found a total of $735 million was paid from Puerto Rico’s public coffers just to cancel interest rate swaps.[19]

Banks like Santander facilitated municipalities’ use of interest rate swaps with the belief they’ll save money, but termination clauses have a high price.

Special purpose entities (SPE’s) were created by the Puerto Rican government as corporate and political entities independent of the Commonwealth of Puerto Rico, in some cases to enable the government to borrow more money. We will focus on an SPE called COFINA, that was set up to issue bonds to pay or refinance certain debts of the Commonwealth.[20] We found that Santander participated as underwriter in over $15 billion of COFINA bond issues between 2007 and 2011.

COFINA bond issues diverted sales taxes that could have been used for economic development in order to pay off bondholders.[21]

COFINA diverted Puerto Rican citizens’ sales tax to bondholders, which could have been used to build schools.

Origins of the Debt Crisis

Puerto Rico’s debt crisis has its roots in multiple factors, including the phasing out of IRS Section 936 that provided a tax benefit to U.S. corporations, over a 10-year period beginning in 1996. According to a former President of the GDB Melba Acosta-Febo, “this crisis is the culmination of decades of ill-advised public policy – both in San Juan and in Washington – coupled with a persistent stagnating economy, seemingly unlimited access to easy credit, and a market willing to lend.”[22]

In 2006, Puerto Rico went into a recession from which it has not recovered. Public debt grew from a sustainable 63% of GNP to just over 100% of GNP by 2015.[23] This was fueled by budget deficits and U.S. investors’ demand for the Commonwealth’s tax-free municipal bonds, which have historically been popular because they are exempt from federal, state, and local taxes and are constitutionally guaranteed by the Puerto Rican government.

Banks like Santander drove demand for Puerto Rico’s triple tax exempt bonds, for example with its series of mutual funds, First Puerto Rico.

The growth of Puerto Rican debt for the past 10 years provided enormous profits for the banks selected by the GDB to underwrite its bonds. These included global banks such as Citigroup, Goldman Sachs, and Merrill Lynch, but also local banks such as Popular, Oriental and Santander. The Wall Street Journal estimated in 2013 that Puerto Rico had issued $61 billion in bonds since 2006, paying Wall Street securities firms, lawyers and others about $1.4 billion in fees.[24] Banks like Santander exacerbated the debt crisis by structuring Puerto Rican bond deals and finding the buyers to scoop them up, for which they received generous fees from the government.

Santander Securities becomes one of the principal bankers to the government

Santander bank was well positioned to benefit from the explosion of public debt in Puerto Rico. In 1996 Santander hired José Ramon Gonzalez to run its investment brokerage start-up, called Santander Securities. Gonzalez, who had served as head of the GDB between 1986 and 1989, built Santander Securities’ business in the Commonwealth, and closely tied its fortunes to the Puerto Rican municipal debt market. While serving as CEO of Santander Securities from 1996-2001, Gonzalez also established a series of mutual funds known as First Puerto Rico, managed in-house by a subsidiary known as Santander Asset Management, which mainly invested in Puerto Rican debt securities.

In 2002, Gonzalez became CEO of the bank’s holding company, known as BanCorp, where he served until 2008, even as he continued to serve as chairman of Santander Securities. His replacement as CEO of Santander Securities was Carlos M. “Kako” Garcia. Garcia joined Santander Securities in 1997 to help Gonzalez create an investment banking operation to do municipal debt underwriting. At Santander Securities, Garcia helped Gonzalez with the acquisition of Merrill Lynch’s island-based brokerage and asset management business and, in his own words, “structured, advised and/or managed debt, equity and M&A transactions…including acting as one of the principal bankers of the Government of Puerto Rico.”[25]

Garcia and Gonzalez built Santander Securities, the bank’s municipal bond business.

Under the direction of Gonzalez and Garcia, Santander Securities quickly established itself as a leading bond underwriter, coinciding with the growth in Puerto Rican public debt. In 2004 Santander helped issue over $6.1 billion in new securities, including a $1.2 billion bond issue for the Puerto Rico Public Finance Corporation. By 2005 Santander’s underwriting business generated nearly 50% of parent BanCorp’s fee income, with most of that coming from Puerto Rican public debt. As the Commonwealth fell into recession in 2006 and borrowed more, Santander Securities participated in the underwriting and structuring of $32 billion in government sponsored debt (between 2006-2009). Fee income alone at Santander Securities rose from $51 million in 2004 to $75 million in 2008 (and $60 million in 2009).[26]

Governor Fortuño enacts austerity and appoints Santander executives to GDB to manage the fiscal crisis

In 2008, the third year of recession in Puerto Rico, the New Progressive Party (NPP) won a landslide election, handing the Governor-elect, Luis Fortuño, super majorities in the Commonwealth’s Legislative Assembly. Fortuño, who caucused with Republicans during his four years as Puerto Rico’s representative to U.S. Congress, campaigned on a program of cutting taxes and shrinking government.

Within months of becoming governor Fortuño got a series of laws passed to implement an austerity program for Puerto Rico called the Fiscal and Economic Recovery Plan. Fortuño’s goal was to stabilize Puerto Rico’s Wall Street credit rating, and provide some economic stimulus through tax cuts and public private partnerships for infrastructure development. At the same time, the government moved to lay off tens of thousands of public employees and to privatize public assets such as the San Juan airport. The economic plan did not lift Puerto Rico out of recession however, and tax revenues continued to decline.

When Governor Luis Fortuño was elected he implemented an austerity plan and appointed Carlos M. Garcia to lead the GDB.

To handle the fiscal crisis, Fortuño brought in Santander’s Carlos M. Garcia to lead the GDB as its Chairman, CEO and President. In turn, Garcia asked Fortuño to establish a private-sector board of directors for the GDB. To run the GDB, Garcia brought in several current or former Santander executives: Jesús F. Méndez, a former Managing Director of Santander Securities; David Alvarez, an analyst at Santander Securities; William Lockwood Benet, former advisor to Santander; George Joyner, former president of Santander Mortgage Corp.; and Fernando L. Batlle,[27] whose brother, Juan Carlos Batlle, replaced Jesús Méndez as managing director of Santander Securities. Among other managers who joined the GDB under Garcia was Ignacio Canto, who arrived in 2010 with experience structuring Puerto Rican public debt deals for Santander Securities.

The Santander team maintained its grip on the GDB throughout the Fortuño administration. In 2011 Juan Carlos Batlle moved from a senior role at Santander to replace Carlos Garcia as the head of the GDB while his brother Fernando left the GDB to become CEO of Santander Securities. This amounted to a virtual revolving door of brothers, rotating between the bond underwriter and the government agency charged with selecting bond underwriters. When Carlos Garcia left the GDB, he returned to Santander where he became executive vice president of the U.S. bank holding company.[28]

Juan Carlos Batlle and his brother were a virtual revolving door of brothers between Santander Securities and the GDB.

The Santander-led GDB aggressively pursues questionable COFINA bonds to maintain Puerto Rico’s credit ratings

With his team in place at the GDB, Garcia moved swiftly to reassure the bond market. In order to maintain Puerto Rico’s credit ratings, Garcia relied on issuance of a new category of municipal debt, secured by regressive Puerto Rican sales and use tax receipts. These “safe” bonds, known by their Spanish language acronym, COFINA, were issued mainly to refund outstanding interest and principal on previously issued government debt, and also provide deficit financing for the Commonwealth.[29]

The legality of COFINA as a separate governmental structure with a dedicated revenue stream to exclusively to pay bondholders has never been determined by a court, although it is the subject of an ongoing federal lawsuit between rival groups of COFINA and General Obligation (GO) bondholders.[30]

Fortuño then had a law passed in January 2009 that doubled the amount of sales tax revenue set aside for COFINA bonds, enabling the Garcia’s GDB to issue more debt underwritten by Santander and other banks. Law 7, passed in March 2009, permitted the Treasury Secretary to refinance debt without considering whether it would actually save Puerto Rico money.[31]

Mass protests in Puerto Rico over layoffs and Public Law 7.

Garcia issues more debt to repay bondholders, earning more fee income for Santander

With the new laws in place, Garcia was able to sell $5.3 billion in COFINA bonds with two issues during 2009. Santander participated as underwriter in both issues, and acted as the lead bank in one. The bonds were used primarily to refinance existing debt, both extending the length and increasing the amounts that would ultimately need to be repaid by Puerto Rico with sales tax revenues.

Each bond issue was also subject to risky financial provisions. For example, COFINA entered into interest rate swap agreements with undisclosed “counterparties,” which are typically Wall Street banks. When Puerto Rico’s bonds were downgraded, it ended up paying termination fees to these parties because the credit downgrade caused it to be in a state of technical default, which caused interest rates swaps to accelerate to default rates. One COFINA bond issuance in 2011 raised money to make a $400 million interest rate swap termination payment, instead of being used to fund Puerto Rico’s healthcare, education or infrastructure development. Santander helped underwrite this bond issue.[32]

COFINA debt also featured capital appreciation bonds or CABs. To cite one example in Puerto Rico, the COFINA 2009A First Subordinate Series issue underwritten by Santander contained CABs that raised $139 million for the government, but the amount due at maturity — compounded at interest rates of between 6.875% and 7.125% — was $730 million, over five times the amount borrowed.[33] If the $139 million borrowed at the same rates would be paid back using simple, not compounded interest, the amount due at maturity would have been only $371 million.

Santander helped underwrite a bond issue to raise money to pay a $400 million interest rate swap termination, which could have been used to fund healthcare or infrastructure.

Some of these debt deals borrowed even more money to pay the interest on the amount owed. This is called capitalized interest. Traditionally, capitalized interest is used to pay bondholders during the construction phase of a project, before it can generate revenue. Once the project is complete, bondholders are paid with the revenue generated from the project. In the case of COFINA bonds however, the only source of income to pay interest would be an increase in sales and use taxes. The use of capitalized interest created more fee income for bond underwriters like Santander who participated in numerous COFINA and other deals that borrowed to pay interest.

In total, COFINA debt deals put together by the GDB under Carlos Garcia and Juan Carlos Batlle were just over $10.8 billion. The GBD also issued $8 billion of its own notes at the direction of Garcia and Batlle, with Santander participating as an underwriter in all of them. The GDB paper has since been downgraded to junk and the bank has defaulted on some of its payments.[34]

Capitalized interest generated more fee income for bond underwriters like Santander who participated in underwriting COFINA and GDB debt deals worth over $18.8 billion.

Garcia and Batlle’s COFINA deals saddled Puerto Rico with additional debt

Analysis of a specific COFINA bond issue from 2011[35] demonstrates how reliant on questionable financial engineering the GDB had become during the Fortuño years. Although the Puerto Rico Constitution says the Commonwealth cannot issue public debt with a maturity of more than 30 years,[36] most of the COFINA 2011A Subordinate Series Bonds mature in 32 to 39 years. The bonds raised $734 million, including $35.2 million for interest. Some of these proceeds were used to retire – prior to maturity – COFINA bonds issued in 2009 and to make separate interest payments on other 2009 COFINA bonds. Santander was an underwriter of these 2009 bonds.

In addition, $337 million of the 2011A First Subordinate Series bonds were issued as CABs and were purchased by the Puerto Rican Infrastructure Finance Authority and the Puerto Rican Employees Retirement System (ERS). These CABs don’t mature for 35-37 years, accrue interest at 7% and have an approximate value of $2.4 billion at maturity, over 13 times the amount borrowed.

Bond underwriters, including Santander, helped sell these bonds. In turn, Santander received a share of the $2.7 million underwriters discount. The bonds were approved by the GDB headed by Juan Carlos Batlle, who joined the GDB from Santander Securities and who also was serving as Vice Chairman of the COFINA corporation when the bonds were issued. His brother was CEO of Santander Securities at the time of this issue.

The GDB became increasingly reliant on questionable financial engineering during the Fortuño years.

Santander also underwrote risky pension deals – did it know better?

When the recession hit Puerto Rico, the underfunded Employee Retirement System (ERS) pension plan issued its own bonds at the direction of the governor, Acevedo Vila, involving Santander and other banks. In 2008 Santander helped underwrite three bond issues using employer contributions as collateral— virtually unheard of for a public pension plan.[37]

The idea was to leverage up to $7 billion so that it could be invested and the interest earned would provide payouts to the plan’s beneficiaries. The bonds were only marketed to Puerto Rican investors due to an alleged lack of international appetite.[38]

Three ERS bond issues raised $2.9 billion, while UBS, Santander and other banks shared $35.7 million in issuance fees. When Fortuño became governor, he declined to allow the ERS to issue more debt, and hired a consultant to analyze his predecessor’s handling of the pension’s finances. The consultant concluded that the bond deals were so “obviously flawed and not logical” that it “could imply a lack of understanding” of the deal by island officials.[39] However, these pension fund bonds were underwritten by Santander Securities when Carlos Garcia was there in a senior role. According to Reuters the consultant’s report was understood by many as a political maneuver.

Nonetheless, this borrowing added to the pension fund’s liability as money is now going to pay off bondholders who will be paid before pensioners.

ERS and Puerto Rico’s Teachers’ Retirement System, covering 330,000 workers and retirees, have liabilities totaling $43.2 billion, while their assets are worth $1.8 billion—a 96% shortfall, reportedly the largest ever for a U.S. state pension. The pensions are forecasted to run out of money in two years.[40]

Santander and other banks earned at least $35.7 million in underwriting fees in three ERS debt deals that used employers’ contributions as collateral, virtually unheard of for public pension funds.

Could Santander and its executives have believed all this debt was affordable?

The GDB’s refinancing, growth and extension of debt under Garcia and Batlle, especially using COFINA bonds, on top of the budget cuts carried out by the Fortuño administration did not save Puerto Rico from catastrophe. It only pushed it out a few years, by massively increasing the amount owed to creditors.

A key question all Puerto Ricans must ask – and banks like Santander should be held accountable for answering – is how did the Commonwealth’s debt grow so much and become so onerous that it became unpayable? For many years now, investment banks and municipal bond advisors like Santander Securities have advised governments like Puerto Rico that issued debt with non-traditional and toxic borrowing structures.

The lure of these structures, including CABs, interest rate swaps, capitalized interest, and establishing off balance sheet corporations like COFINA with separate revenue streams to borrow more from, is that they allow banks and governments to act as if nothing is amiss, permitting the banks to profit from an ever increasing number of transactions under ever more problematic terms and conditions.

Conclusion

A crushing debt burden was placed on the Puerto Rican people with the assistance of bankers like Santander—making economic growth for the island almost impossible without some debt cancellation. Santander advised, structured and arranged much of this debt that linked investors eager for tax-free profits with desperate governments that were facing ruin.

A crushing debt burden was placed on the Puerto Rican people with the assistance of bankers like Santander Share on XSantander should refund all the underwriting fees and discounts it received from the government, including its public corporations and instrumentalities like COFINA. Too much of the debt Santander underwrote was questionable or underwritten when the bank had conflicted relationships with the government. José Ramon Gonzalez and Carlos Garcia should resign from the Fiscal Control Board. As architects of the debt crisis, they should not be put in positions of power to adjudicate its outcome.

Caption: A key question all Puerto Ricans must ask – should banks like Santander be held accountable for their role in Puerto Rico’s debt crisis?

Last but not least, many questions remain about the creation of Puerto Rico’s debt and whether it all the debt is legitimate. We support the ongoing work of the Puerto Rico Commission for the Comprehensive Audit of the Public Credit (Audit Commission). The Audit Commission should be funded and empowered to complete its investigation of the debt, so that Puerto Rican people are provided with answers.

Footnotes

[i] “Oversight Board Director Owns at Least $265,000 in Puerto Rico Bonds,” Bond Buyer, 03-06-2017.

[ii] “P.R. Opposition Leader Says Board’s Financial Disclosures May Require Resignations,” Bond Buyer 03-09-2017.

[iii] http://www.cfgcompany.com/company

[iv] For the law governing interest rates see Reglamento Num. 5782 Para Disponer Sobre Las Tasas De Interes y Otros Asuntos en la Concesion de Prestamos Personales Pegquenos here: http://www.ocif.gobierno.pr/documents/5782.pdf . ‘No se fija una tasa de interes anual maxima’ means ‘no maximum annual interest rate.’ For small loans made in Puerto Rico last year see the Office of the Commissioner of Financial Institutions report on small loans companies here: http://www.ocif.gobierno.pr/documents/Q2-2013/small_loan_co.pdf

[v] http://www-03.ibm.com/software/businesscasestudies/us/en/corp?synkey=P367392I18175V50

[vi] Financial Information – Carlos Garcia,” pg. 2, available at https://juntasupervision.pr.gov/index.php/en/documents/

[vii] https://www.sec.gov/Archives/edgar/data/1665581/000090866216000483/xslFormDX01/primary_doc.xml

[viii] Financial Information – Carlos Garcia,” pg. 2, available at https://juntasupervision.pr.gov/index.php/en/documents/

[ix] http://bayboston.com/#/team/caribbean-financial-group-holdings-l-p

[1] We use Santander to mean Banco Santander, SA, and all its affiliates. In Puerto Rico, for much of the period of time covered in this report, Santander BanCorp was the parent bank holding company for Banco Santander Puerto Rico, which had several subsidiaries including Santander Securities Corp., Santander Asset Management, Santander Mortgage Corp., Santander Insurance Agency, Santander International Bank, Santander Financial Services (also known as Island Finance), Island Insurance Corp., and Santander Puerto Rico Capital Trust I.

[2] The legality of COFINA as a separate governmental structure with a dedicated revenue stream to exclusively to pay bondholders has never been determined by a court.

[3] For example, in October 2015, Financial Industry Regulatory Authority (FINRA), the securities industry’s self-regulator, found that Santander didn’t accurately reflect the dangers associated with the Puerto Rican bonds in its

risk-classification

tool. FINRA fined Santander $6.4 million, which was comprised of a $2 million fine and $4.4 million in restitution to customers that purchased Puerto Rican bonds. See: http://www.finra.org/newsroom/2015/finra-sanctions-santander-64-million-pr-bond-supervisory-failures

[4] The GDB is bank, fiscal agent and acts as

financial

advisor for the Commonwealth of Puerto Rico, and its instrumentalities (public corporations and municipalities) in connection with all their borrowings. All

such borrowings are subject to approval by GDB. The GDB also selects bond underwriters in connection with issuing bonds.

[5] See “GDB locks up the piggy bank,” Caribbean Business, 01-29-2009.

[6] See for example Refund America, “Puerto Rico’s Payday Loans.” See also Tom Sgouros, “Predatory Public Finance,” The Journal of Law in Society, Vol. 17:1 (2014).

[7] See Diane Lourdes-Dick, “U.S. Tax Imperialism,” The Seattle University School Digital Law Commons (2015). According to Lourdes-Dick, Puerto Rico’s ambiguous political status and inability to restructure its debt (even though Puerto Rico attempted to give itself that authority with legislation in 2016) are partly responsible for the fiscal crisis, and Wall Street saw the crisis as an opportunity. These two conditions have created a Puerto Rican debt problem that is unique, cyclical, and unresolvable, yet one in which Wall Street bankers have seized on the crisis as both a business opportunity and as policymakers.

[8] Nazario, ed. “Poverty in Puerto Rico: A socioeconomic and demographic analysis with data from the Puerto Rico Community Survey (2014).”

[9] See https://www.whitehouse.gov/sites/default/files/docs/puerto_rico_hill_update_0419.pdf

[10] We analyzed bond issues’ Official Statements taken from EMMA and the GDB website, 2000 to present, in which Santander was lead or participating underwriter, with the addition of several Industrial, Tourist, Educational, Medical and Environmental Control Facilities Financing Authority (

AFICA

) bonds from the late 1990s. Each bond was examined for the listed underwriters on the cover, whose role and importance are generally denoted by the size of font and order in which they’re listed. If Santander was listed first or among the first three underwriters listed, we determined this was a lead or co-lead underwriting role. If Santander was listed anywhere else, we determined them to be a participating underwriter. On the second page,

tranches

in the bond issue are generally listed which denote whether the issue contained CABs, the amount of CAB principal, and usually their worth at maturity and yield rate. Bonds’ Official Statements were then scanned for their sources and uses of funds or plans of financing which generally list underwriting fees, costs of issuances and underwriters’ discounts as well as other fees, capitalized interest, or interest rate swap termination payments.

Usually

this section is called “Sources and Uses of Funds,” “Plan of Financing,” or is in “Underwriting.”

[11] The 2006 law establishing COFINA limited its legal purpose to issuing bonds or other financial mechanisms to pay or refinance Puerto Rico’s extra-constitutional debt. In our analysis of 90 bonds we found the use of these techniques to peak in: CABs (2008), capitalized interest (2011-2012), and swap agreements payments (2012).

[12] See https://medium.com/@munilass/how-state-and-local-governments-use-financial-engineering-to-game-their-debt-burdens-the-new-68a155e7ab31#.wqv0h5gud

COFINA

(9), ERS (3), PRPFC (3), PRHFA (2), PRIDCO (1), PRASA (1) and GDB (1).

[14] ReFund America, “Scooping and Tossing Puerto Rico’s Future,” p. 6.

PREPA

(8), COFINA (6), GDB (4), PRASA (3), PRPBA (3), PRPFC (3),

AFICA

(1), ERS (1),

PRIFA

(1).

[16] This is a useful example of an interest rate swap is provided from moneycrashers.com: “ABC Company and XYZ Company enter into one-year interest rate swap with a nominal value of $1 million. ABC offers XYZ a fixed annual rate of 5% in exchange for a rate of LIBOR plus

1%,

since both parties believe that LIBOR will be roughly 4%. At the end of the year, ABC will pay XYZ $50,000 (5% of $1 million). If the LIBOR rate is trading at 4.75%, XYZ then will have to pay ABC Company $57,500 (5.75% of $1 million, because of the agreement to pay LIBOR plus 1%). Therefore, the value of the swap to ABC and XYZ is the difference between what they receive and spend. Since LIBOR ended up higher than both companies thought, ABC won out with a gain of $7,500, while XYZ realizes a loss of $7,500. Generally, only the net payment will be made. When XYZ pays $7,500 to ABC, both companies avoid the cost and complexities of each company paying the full $50,000 and $57,500.

[17] Wall Street Journal, “Banks Rack Up Big Fees from Puerto Rico Bond Deals”, 10-23-2013.

[18] Puerto Rico Commission for the Comprehensive Audit of the Public Credit Pre-Audit Survey Report, p. 13.

COFINA

(2), GDB (4), PRASA (1),

PRIFA

(1), PRPBA (1).

[20] Standard and Poor’s, Global Credit Portal Ratings Direct, “Puerto Rico Sales Tax Financing Corp.; Sales Tax,” June 28,

2007

p. 2

[21] See for example Garcia’s presentation at the Puerto Rican Credit Conference in 2009, http://www.gdb-pur.com/pdfs/CREDCONFFEB-20-09.pdf, pp 94-95. A law increased

the amount of

sales and use tax went to COFINA to refinance debt.

[22] Statement of Melba Acosta-Febo, on behalf of the Government Development Bank for Puerto Rico, before the U.S. Senate Finance Committee, 9-29-2015.

[23] Krueger,

Teja

and Wolfe, “Puerto Rico: A Way Forward,” 6-29-2015, p. 9.

[24] Wall Street Journal, “Banks Rack Up Big Fees from Puerto Rico Bond Deals”, 10-23-2013.

[25] See Garcia’s resume here: http://democrats-naturalresources.house.gov/imo/media/doc/garcia_testimony_updated_2_3_16.pdf

[26] Information provided by Santander BanCorp annual reports. In 2010 Santander

BanCorp

became a wholly-owned subsidiary of Banco Santander, S.A. and ceased filing annual reports with the S.E.C.

[27] See “GDB locks up the piggy bank,” Caribbean Business, 01-29-2009.

[28] See Garcia’s resume: http://democrats-naturalresources.house.gov/imo/media/doc/garcia_testimony_updated_2_3_16.pdf. It says he was responsible for strategic projects to develop the U.S. banking franchise including a rebranding to Santander from Sovereign in 2013.

[29] Detailed in Garcia’s presentation at the Puerto Rican Credit Conference in 2009, http://www.gdb-pur.com/pdfs/CREDCONFFEB-20-09.pdf.

[30] The lawsuit is Lex Claims, LLC et.al. v. the Commonwealth of Puerto Rico, U.S. District for Puerto Rico, Case 3:16-cv-02374-FAB.

<sup[31] Law 7, Chapter IV, Section 47. Refinancing bonds were exempted from the requirements of Section 3 (f)(3) of 13 L.P.R.A. § 141b, which states that “no refinancing bonds shall be issued unless the Secretary of the Treasury shall have first determined that the present worth of the aggregate principal and interest on the refinancing bonds is less than the present worth of the aggregate principal and interest on the outstanding bonds to be refinanced; for the purposes of this limitation…”

[32] See Puerto Rico Commission for the Comprehensive Audit of the Public Credit Pre-Audit Survey Report, p. 13, and for COFINA interest rate swap termination payment see http://emma.msrb.org/ER535765-ER414252-ER816052.pdf, pp 39, for another example, see http://emma.msrb.org/ER536037-ER414248-ER816051.pdf, pp 43-44.

[33] See http://emma.msrb.org/EA283776-EA2574-EA571322.pdf. See

description

of Capital Appreciation Bonds here, the author estimates that 63% of Puerto Rico’s total CAB debt belongs to COFINA.

[34] “Puerto Rico plays brinksmanship with historic debt default,” Institutional Investor, 05-04-2016.

[35] For a description of the bonds discussed in the following two paragraphs, see http://emma.msrb.org/ER536037-EP457350-EP857362.pdf.

[36] Audit commission report, page 23.

[37] See Senior Pension Funding Bonds Series A http://www.gdb-pur.com/pdfs/public_corp/PensionBondsOS-Jan08-final.pdf, Series B http://www.gdb-pur.com/investors_resources/documents/2012-04-09-FinalOS-POBSeriesB.pdf, and Series C http://www.gdb-pur.com/investors_resources/documents/ERSSeniorPensionFundingBonds-SeriesC_000.pdf.

[38] http://www.reuters.com/investigates/special-report/usa-puertorico-pensions/

[39] Ibid.

[40] Ibid.